by George Turner | Jun 7, 2022

Taxation magazine recently carried an article from our Executive Director looking at HMRC’s record on tackling marketed tax avoidance schemes over the last 10 years. The article looks at the differing results HMRC has achieved going after two different types of...

by George Turner | Mar 21, 2022

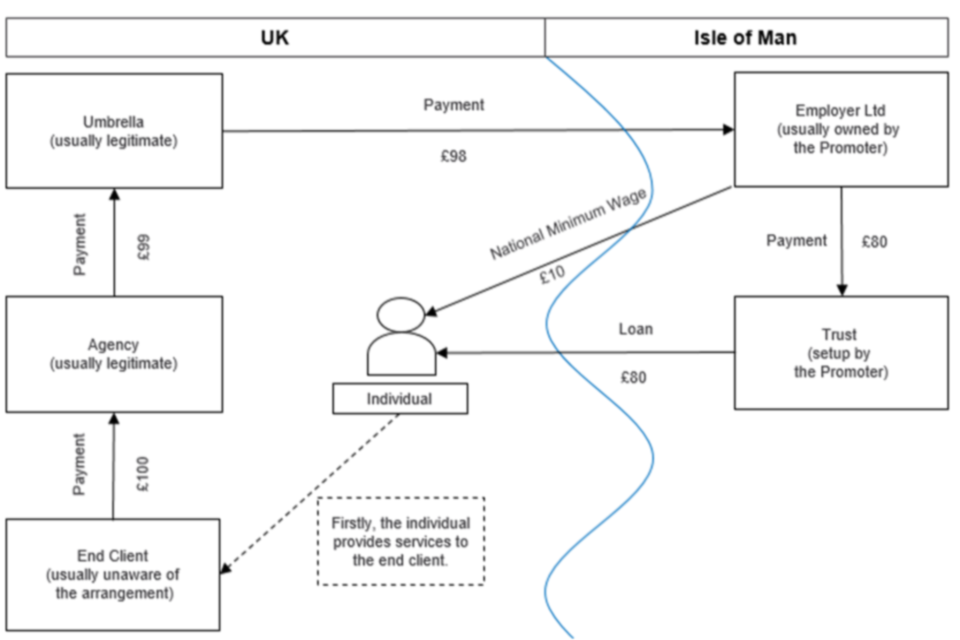

TaxWatch has lodged a complaint concerning Arthur Lancaster, Director of AML Tax (UK) Limited, and Director of the Knox House Trust of the Isle of Man. Mr Lancaster is both a member of the Chartered Institute of Taxation and the Institute of Chartered Accountants of...

by George Turner | Feb 14, 2022

HMRC’s record on tax fraud has been questioned by two select committees and in several parliamentary debates in recent weeks The last select committee inquiry on Tax Fraud was in 2015 Recent weeks have seen HMRC being put under intense scrutiny on their record on...

by George Turner | Jan 27, 2022

TaxWatch has submitted a complaint to the Tax Disciplinary Panel about the conduct of an individual identified as “Mr Red” in the case of Murray Group Holdings vs HMRC. TaxWatch believes that it has managed to uncover the identity of Mr Red, who continues to practice...

by George Turner | Dec 7, 2021

New analysis shows that the number of users of disguised remuneration schemes has increased dramatically despite government attempts to legislate against the schemes Criminal investigations against promoters remain a rarity, with no successful prosecutions being...