by George Turner | Jan 27, 2022

TaxWatch has submitted a complaint to the Tax Disciplinary Panel about the conduct of an individual identified as “Mr Red” in the case of Murray Group Holdings vs HMRC. TaxWatch believes that it has managed to uncover the identity of Mr Red, who continues to practice...

by Alex Dunnagan | Jan 19, 2022

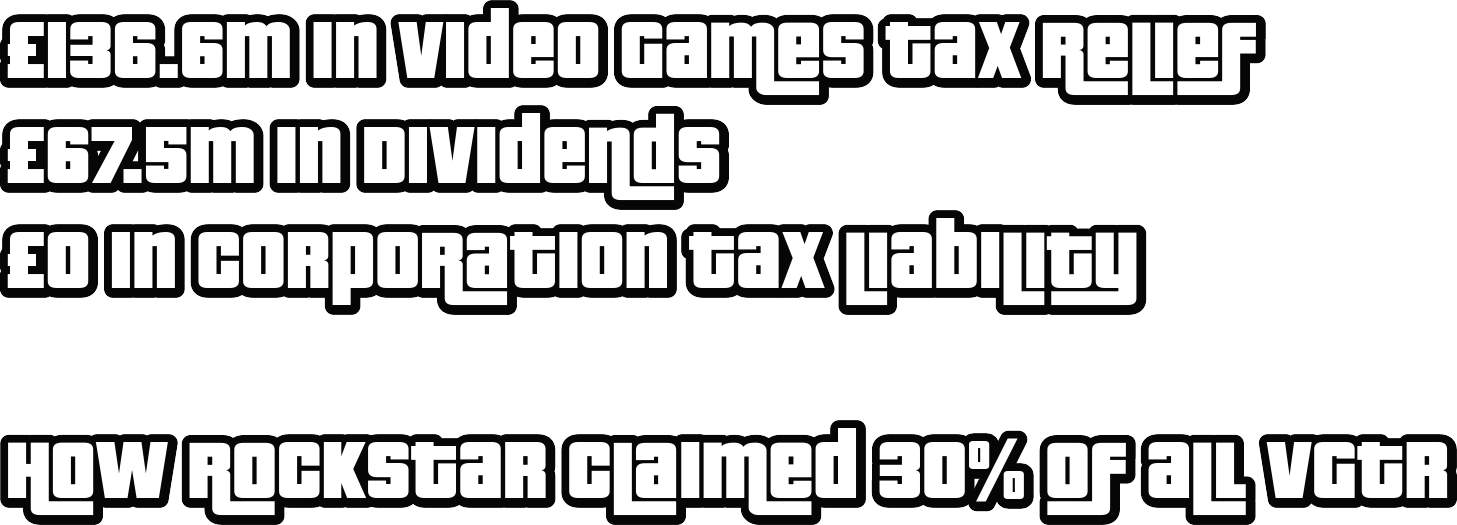

Rockstar Games UK Limited (previously Rockstar North) has finally published it’s 2020 accounts, more than one year late. In fact, the publication of Rockstar’s accounts are so late that the company’s 2021 accounts are already overdue. The recently filed 2020...

by Alex Dunnagan | Jan 17, 2022

Three-quarters of Covid support claimed in fraud and error won’t be collected HMRC has revealed that they expect to recover just 25% of a total £5.8bn paid out due to fraud and error in relation to the coronavirus support schemes. 1HMRC responses to inaccurate claims,...