by Alex Dunnagan | Jan 27, 2023

Video Games Tax Relief (VGTR) cost a record £197m last year, more than five times as much as it was anticipated to cost when it was introduced.1 A total of £830m in subsidy to the video games industry has been paid since the relief was introduced, with numbers...

by Alex Dunnagan | May 9, 2022

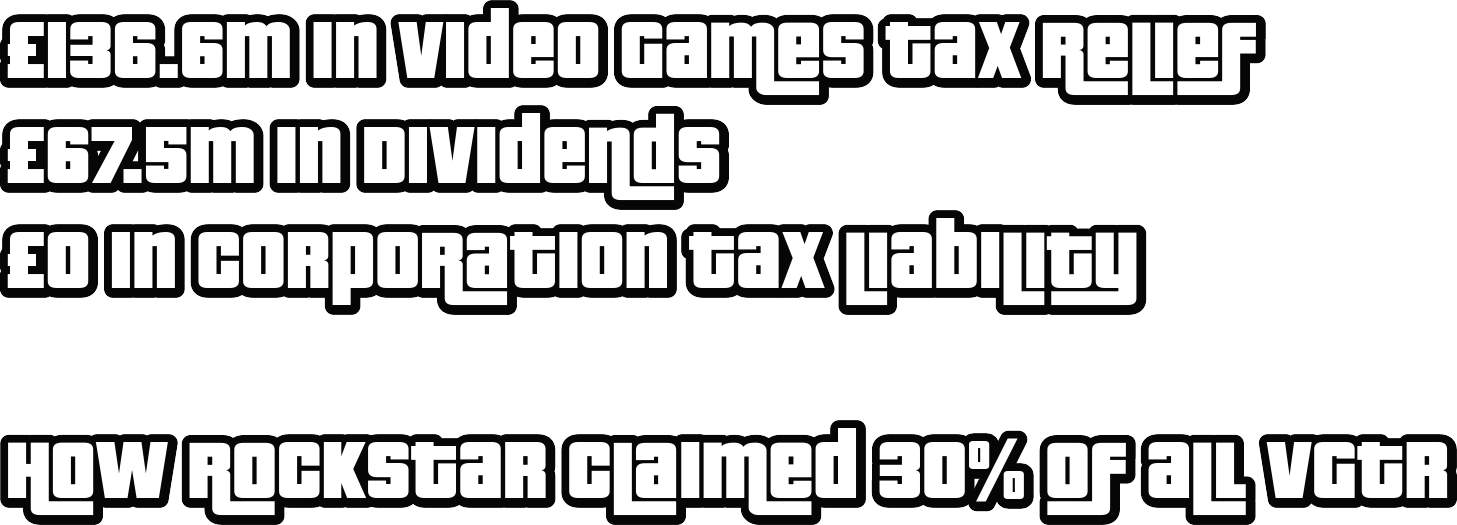

Rockstar Games has revealed that they claimed £68.4m in Video Games Tax Relief (VGTR) in 2020-2021, equivalent to 38% of the entire amount of VGTR paid out that year. The amount Rockstar are claiming is rising every year, taking the total the US-owned company has...

by Alex Dunnagan | Jan 19, 2022

Rockstar Games UK Limited (previously Rockstar North) has finally published it’s 2020 accounts, more than one year late. In fact, the publication of Rockstar’s accounts are so late that the company’s 2021 accounts are already overdue. The recently filed 2020...

by Alex Dunnagan | Oct 14, 2021

Key facts and figures: £180m paid out in VGTR last year 48% increase in VGTR on the previous year 55 claims for over £500,000 represent 87% of the total value of payments Video Games Tax Relief (VGTR), a form of subsidy to the UK videogames industry, has seen a 48%...

by Alex Dunnagan | Jan 19, 2020

Rockstar North, the Edinburgh based company behind the wildly successful Grand Theft Auto series, has published its latest accounts, revealing a huge increase in claims for Video Games Tax Relief. As reported in today’s Sunday Telegraph, analysis by TaxWatch...