by Mike Lewis | May 14, 2025

The government wants to step up the fight against enablers of tax abuse (again). New powers and better information can help. But HMRC is barely using some of the powers and penalties it already has. *** Laws that aren’t enforced are simply polite recommendations....

by Claire Aston | Oct 24, 2024

£300 million tax lost to non compliance by UK resident individuals on offshore accounts in 2018-19 This figure appears to be a gross underestimate, definitely excluding any assets held through companies, and the treatment of assets within trusts isn’t clear...

by Claire Aston | May 15, 2024

Multiple delays to the publication of the offshore tax gap statistics, now a full year late TaxWatch had to use FOI powers to discover that the new date for this work is now June 2024 (gov.uk still shows Autumn 2023) Data on which this will be based is from CRS...

by George Turner | Dec 7, 2021

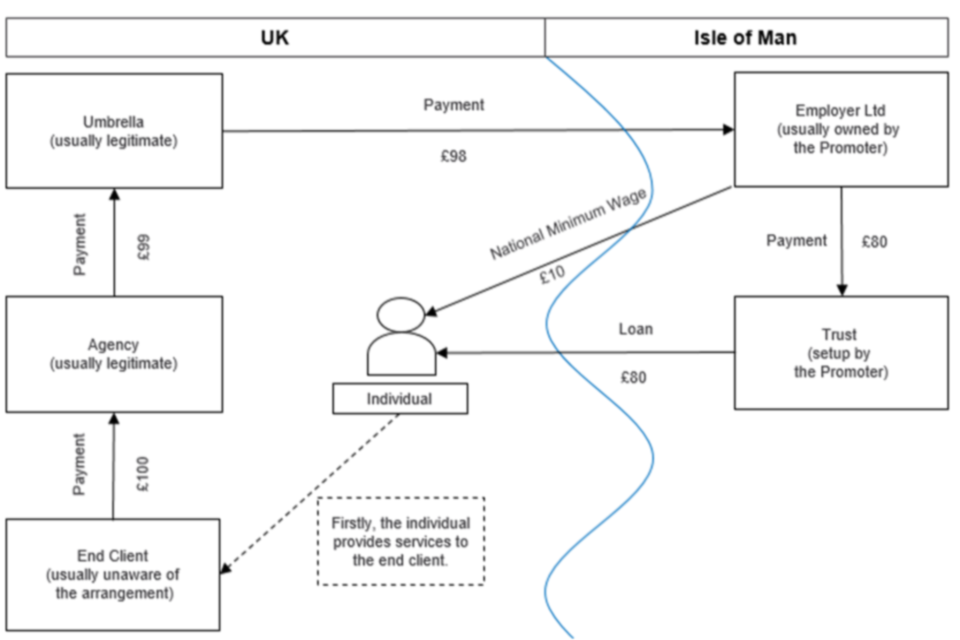

New analysis shows that the number of users of disguised remuneration schemes has increased dramatically despite government attempts to legislate against the schemes Criminal investigations against promoters remain a rarity, with no successful prosecutions being...

by Alex Dunnagan | Dec 1, 2021

The Finance Bill 2021-22 was published earlier in November, legislating for tax changes announced at the Autumn Budget. This briefing focuses on two aspects of the bill, amendments to the Diverted Profits Tax and measures relating to the promotion of tax avoidance...