by Dr Pete Sproat | Apr 24, 2023

In 2016 Chancellor George Osborne declared the introduction of the loan charge would “shut down disguised remuneration schemes”. Yet HMRC estimates 31,000 people used such schemes in 2020-21, resulting in a loss of £400m in tax. The authorities have attempted to...

by George Turner | Mar 21, 2022

TaxWatch has lodged a complaint concerning Arthur Lancaster, Director of AML Tax (UK) Limited, and Director of the Knox House Trust of the Isle of Man. Mr Lancaster is both a member of the Chartered Institute of Taxation and the Institute of Chartered Accountants of...

by George Turner | Dec 7, 2021

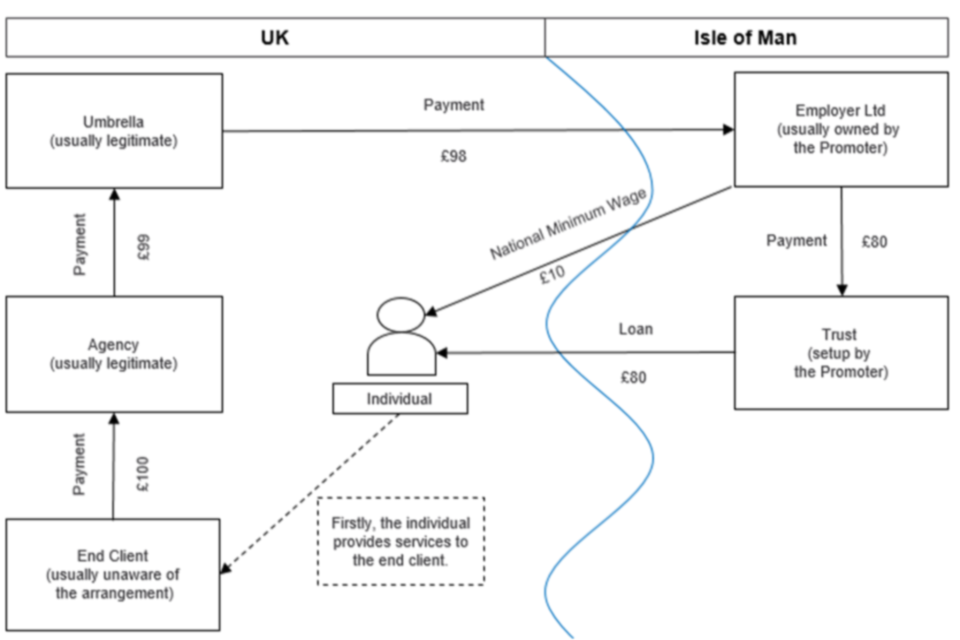

New analysis shows that the number of users of disguised remuneration schemes has increased dramatically despite government attempts to legislate against the schemes Criminal investigations against promoters remain a rarity, with no successful prosecutions being...

by Alex Dunnagan | Oct 2, 2020

TaxWatch Executive Director, George Turner, has written to HMRC calling for those who sell disguised remuneration tax avoidance schemes to be investigated for tax fraud. We have previously written to the Economic Crime Unit of the City of London Police, calling on the...

by Alex Dunnagan | Aug 19, 2020

TaxWatch is calling on the Economic Crime Unit of the City of London Police to open a fraud investigation into the promoters and marketers of disguised remuneration tax avoidance schemes. Recent press reports have revealed that disguised remuneration tax avoidance...