by George Turner | Jun 5, 2019

The European Commission has replied to TaxWatch’s call to launch an investigation into the tax structure of Google. The Commission has said it will consider the information provided by TaxWatch as part of its ongoing investigation into tax agreements in Ireland and...

by George Turner | Apr 26, 2019

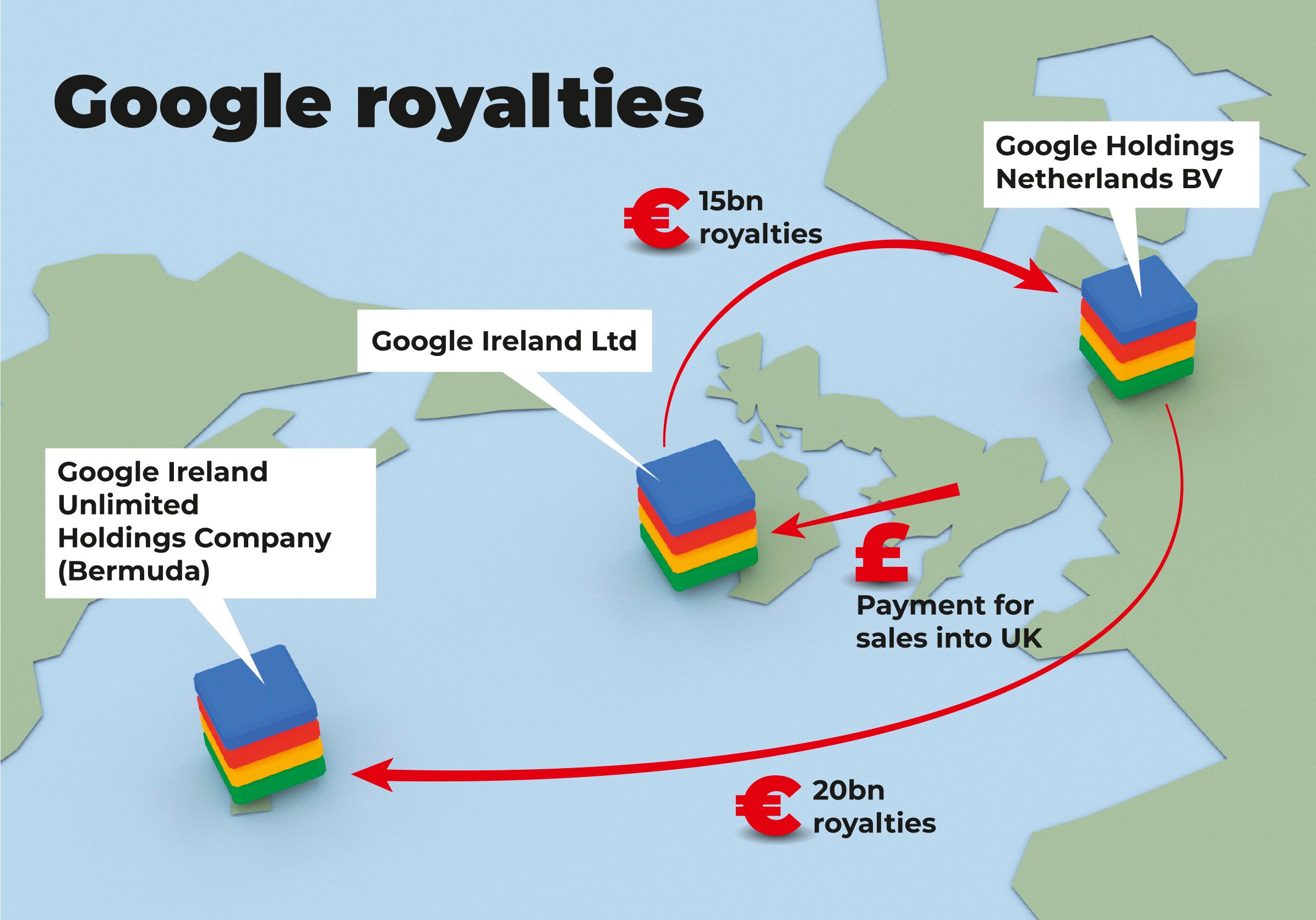

TaxWatch has today written to Commissioner Vestager requesting that the European Commission open an investigation into Google’s European Tax Avoidance scheme, the Double Irish Dutch Sandwich, and specifically whether the Dutch and Irish Governments have provided state...

by George Turner | Nov 6, 2018

How should profit be distributed within the modern multinational corporation? That is the key question at the heart of the debate on international tax avoidance, and one touched on by Taxwatch’s first report. The aspiration of the OECD reforms to the international...