- 3.8m tax returns outstanding a week before the deadline

- Taxpayers spent 6 million hours waiting on the phone in 2022-23

- And 2 million hours waiting on the phone in first 8 months of 2023-24

- 22 minutes average wait time for HMRC to answer calls this year

- £100m+ opportunity cost of call waiting time for taxpayers

HMRC’s increasingly poor telephone service is impacting its ability to collect the right amount of tax and damaging the wider economy due to the level of opportunity costs lost by taxpayers and tax advisers spending time on the phone.

Introduction

In the first of a short series of blogs about the current state of tax administration and compliance, we look at the difficult issue of HMRC customer service, in particular relating to phone calls. Problems with the phone service provided to taxpayers and their representatives have existed for many years, to the extent that they are almost now accepted as a fact of life. The problems must be recognised as arising in the context of reducing real time spending on customer service with actual spending only approaching 2016-17 figures in 2022-23 despite 28% total inflation over that same period. Here we look at what this currently means for taxpayers, businesses and their tax advisers, and the impact on the ability of HMRC to collect the right amount of tax.

Statistics

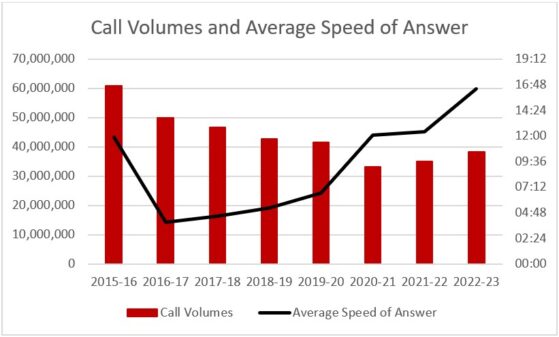

| Calls | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | 2022-23 |

| Call Volumes (m) | 60.8 | 49.9 | 46.7 | 42.7 | 41.6 | 33.3 | 35.2 | 38.3 |

| Average Speed of Answer | 11:54 | 03:54 | 04:28 | 05:14 | 06:39 | 12:04 | 12:22 | 16:24 |

| % of call attempts handled by Contact Centres | 71.6 | 91.7 | 87.1 | 84.1 | 79.4 | 73.6 | 82.3 | 72.5 |

The table/chart above shows that call volumes have unsurprisingly dropped since the middle of the last decade, from around 60 million in 2015-16 to 38 million in 2022-23 due to provision of multiple online services. However, call numbers have been creeping up again since 2020-21 and the average length of time to answer calls has consistently increased since 2016-17 hitting over 16 minutes in 2022-23. This means that, for those calls that did get through, callers had spent 7.6 million hours waiting for the phone to be answered.

And that is only in relation to those calls that got through. Only 73% of attempts to call were actually handled, the remaining 27% being cut off or abandoned. No data is provided for how long those callers wait on average but that will only add to the wasted time for taxpayers.

Most recently published year-to-date data for year to November 20231https://www.gov.uk/government/publications/hmrc-monthly-performance-report-november-2023 and https://www.gov.uk/government/publications/hmrc-monthly-performance-report-november-2022 shows a slight increase in calls compared with the same period in 2022-23. The failed calls rate means that out of just under 25m calls at that point in the year, almost 7m were not answered. In addition, average call waits had increased significantly again to over 22 minutes. This means 7.2m hours of time had already been wasted waiting for the phone to be answered between April and November 2023 with the busiest couple of months in the SA timetable not covered by available statistics.

This decreasing performance is in direct contrast to HMRC’s target to reduce demand for phone services by 30% from 2021-22 to 2024-252https://committees.parliament.uk/oralevidence/14126/pdf/ which would mean call numbers reducing to 24.6m.

Why are we here?

HMRC was in a similar situation in 2015-16 which was recognised as due to a significant reduction in staff numbers following budget pressures3https://assets.publishing.service.gov.uk/media/5a81e74ae5274a2e8ab56736/HMRC_Annual_Report_and_Accounts_2016-17__print_.pdf (Para 15 PR9). This was rectified by investment in new staff and the table/chart above shows the resulting improvement in performance.

Percentage falls in total customer service staff since 2016-17 roughly match falls in the number of phone calls. However, customer service staff are also used to deal with correspondence and webchat. Levels of correspondence have fallen much less than phone calls, and webchat use has increased, so moving staff into those roles is likely to have proportionately reduced the staff available for phone calls.

It must be recognised that significant recent investment in online services brought about a reduction in call volumes relating to more simple enquiries. But we also know that stagnating tax thresholds and other legislative changes mean there are more taxpayers and an increasing proportion have more complex situations, e.g. the rise in the gig economy. This is recognised as an issue by HMRC4https://committees.parliament.uk/oralevidence/13689/pdf/ (Q261) but they are not receiving any additional budgetary resources to deal with their ever-increasing customer base.

Reports from tax professionals and other affected parties suggest that current IT services cannot handle more complex queries and a proportion of calls relate to mistakes made by HMRC5https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels Q15 or chasing responses to other forms of communication6https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels Q14 which can become a vicious circle.

HMRC response

Recognising the falling performance levels of its telephone service, HMRC has generally responded by trying a range of actions to force taxpayers into online services in order to live within its constrained resources.

In particular, HMRC has actively restricted or removed the available phone services at different points in the year, often with little notice. On 22 May last year HMRC closed the VAT registration helpline7https://www.accountingweb.co.uk/any-answers/hmrc-closing-down-the-vat-registration-helpline.The Self-Assessment helpline closed from 12 June to 4 September last year with only three days’ notice given8https://taxaid.org.uk/hmrc-announces-temporary-closure-of-its-self-assessment-helpline. They scrapped the 10-minute waiting time service level agreement for the Agent Dedicated Line (ADL) from 2 October, effectively recognising that they couldn’t meet that target9https://www.theaccountant-online.com/news/icaew-hmrc-service-standard-announcement-signals-new-low/?cf-view. On 7 December HMRC announced that, from 11 December to the SA deadline on 31 January 2024, they would be screening calls to the SA helpline and ADL to answer only those deemed to be a priority10https://www.accountingweb.co.uk/tax/hmrc-policy/restrictions-to-hmrcs-helplines-raise-concerns.

The closure of the SA helpline was presented as a trial by HMRC to look at where the callers would go in the absence of that facility as they accept that they are not resourced to provide the telephone service that is currently demanded and need to find ways to move more people into digital channels11https://committees.parliament.uk/oralevidence/13689/pdf/ Q246+. They admit that greater numbers than anticipated contacted their online services helpdesk and specialist extra support team as a result of this, but other outcomes have not yet been published.

While it is easy to be critical of any restriction of services, HMRC needs to use its resources as efficiently as possible. The restrictions on the SA helplines in the run up to the deadline might be frustrating for many people trying to chase up responses or refunds, but there is an online tool for getting this information and it is at least arguable that tax advisers should be capable of using this. With one week to go before the SA deadline, HMRC reported that 3.8m returns (out of 12.1m) were still outstanding. It therefore doesn’t seem unreasonable for HMRC to focus on providing services to those facing the imminent SA deadline in the absence of additional resources to call on.

Consequences

The performance statistics above show that HMRC telephone services are continuing to deteriorate. Tax professionals, professional bodies and parliamentary committees are all expressing concern at the impact this is having on individuals, businesses and advisers.

Interestingly, the 2016-17 Annual Report and Accounts estimates the opportunity costs saved for callers by reducing call waits from 12 minutes to 4 minutes at £73m12https://assets.publishing.service.gov.uk/media/5a81e74ae5274a2e8ab56736/HMRC_Annual_Report_and_Accounts_2016-17__print_.pdf R10 para 16.. Call waits are currently averaging over 22 minutes so far this year. Even with reduced total numbers of calls, once inflation is taken into account, it doesn’t seem unreasonable to estimate current lost opportunity costs to callers at over £100m a year.

In addition, the inability for people to get answers to their questions must be impacting the level of voluntary compliance and HMRC’s ability to collect the right amount of tax.

Is forcing people into online services the right approach?

HMRC seems to be attempting to force people into using their digital channels, even when they are not adequate for the range of complex issues which arise13 … Continue reading. At a recent Public Accounts Committee hearing, Angela McDonald confirmed that, to keep within their allocated resources and meet their customer service targets, HMRC need to reduce caller demand by 30%14https://committees.parliament.uk/oralevidence/14126/pdf/ Q85 – Q90 and that a range of different approaches are being taken to move taxpayers onto digital services where available. However, she referred to ‘insisting’ that taxpayers use digital services, pointing out that significant numbers of calls relate to simple requests such as tax codes, National Insurance numbers and resetting passwords.

The world is obviously moving towards digital interactions in all spheres, and HMRC needs to use its resources as efficiently as possible. However, it must be recognised that there are important differences between HMRC and private businesses that they may be compared with, such as banks. Banks, retailers and other businesses can persuade people into using online services by removing other options because they make a judgement decision about impact on customers, cost/benefit, competition from others etc. In those circumstances customers have a choice where to go.

HMRC is the only provider of tax administration services, so arguably should not treat taxpayers in the same way. The attitude that taxpayers must be forced to use digital channels misjudges many taxpayers’ positions – those that are digitally able will do what they can online. A recent survey by the Chartered Institute of Taxation (CIOT) suggested that the vast majority of attempted contacts could not be dealt with online but that the caller would use online services to resolve the matter if it was available15https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels. While the survey mainly covered advisers, who are likely to be more used to technology, it is common sense that anybody who feels comfortable with online services would use them rather than hanging on the phone for ages. Those that are less able need encouragement/ persuasion and education, not to be forced into something that they are unsure about. This particularly applies if they are worried about getting things wrong and want the reassurance from a person that they have done the right thing, provided all of the right information etc.

Online services can often feel like a one-way black hole – the CIOT survey indicated that a lot of attempts to contact HMRC were to chase up things submitted online. With increasing publicity about failures of government institutions to treat people fairly in a range of extreme circumstances it is understandable that people want personal reassurance.

It should also be recognised that the need for many calls arise out of apparent mistakes made by HMRC, delays in dealing with correspondence/applications/refunds or poor communication that is not easily understood. Significant staff cuts in some areas of HMRC, for example 1,143 fewer customer services staff in post, (a reduction of over 5%), in the year to December 202316HMRC’s customer service staff numbers revealed (rsmuk.com) will almost certainly have contributed to this. Were staff reductions prioritised over service quality, ultimately hampering overall efficiency? So far the combination of a broader customer base with more complex affairs means that hoped for decreases in demand have not happened – the approaches tried so far do not appear to be working.

Alternatives

It feels like the lessons from the middle of the last decade were not learnt and customer service staff were cut before adequate IT systems were in place that taxpayers were comfortable with using. At this stage the following would seem to be some options for helping to reduce the detrimental effect of HMRC’s poor service on taxpayers and the economy as a whole:

- Additional investment in customer service staff to help educate callers who could use online systems and to clear backlogs of other work that are the cause of some calls

- Using alternative communication options to give clear guidance about whether taxpayers need to contact HMRC or register for self-assessment to pre-empt queries before they arise – one example is providing some text to include on annual interest statements sent by banks to account holders about the Personal Savings Allowance

- Clearer guidelines for taxpayers with simpler affairs who do not fall within self-assessment but have other untaxed income (e.g. state pension recipients)

- Consulting with advisers to understand the most common mistakes made by both HMRC and advisers/taxpayers to enable ways to correct

- Review of issues which result in disproportionate numbers of unnecessary calls, eg. people receiving emails reminding them of upcoming tax return deadlines when they have already submitted

- A call back system at peak times like that operated by some banks and other businesses – potentially enables peaks and troughs in use of phone service to be balanced

Conclusion

Government needs to reflect that HMRC is in the unique position of being essential to administer the tax system and ultimately collect the tax revenues due to the Exchequer, upon which the rest of public spending and service delivery depends. Without a properly functioning, customer focussed, tax administration there are significant consequences for overall UK public finances.

Fundamentally, administration of the tax system needs to make it as easy as possible for taxpayers to get things right. The above shows how current phone and other services are failing to meet the increasing demand for support from taxpayers and advisers, and that attempts to force people into digital channels still seem to be floundering. This failing service appears to be affecting users so badly that it is potentially impacting on economic performance of businesses and advisers. In addition, there is a real risk to long term levels of compliance if taxpayers, businesses and advisers are unable to get adequate responses. This results in the double whammy of impacting HMRC’s ability to collect the right amount of tax and damage to the wider economy which, at a time of financial crisis, is an issue that urgently needs to be addressed.

References

| ↑1 | https://www.gov.uk/government/publications/hmrc-monthly-performance-report-november-2023 and https://www.gov.uk/government/publications/hmrc-monthly-performance-report-november-2022 |

|---|---|

| ↑2 | https://committees.parliament.uk/oralevidence/14126/pdf/ |

| ↑3 | https://assets.publishing.service.gov.uk/media/5a81e74ae5274a2e8ab56736/HMRC_Annual_Report_and_Accounts_2016-17__print_.pdf (Para 15 PR9 |

| ↑4 | https://committees.parliament.uk/oralevidence/13689/pdf/ |

| ↑5 | https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels Q15 |

| ↑6 | https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels Q14 |

| ↑7 | https://www.accountingweb.co.uk/any-answers/hmrc-closing-down-the-vat-registration-helpline |

| ↑8 | https://taxaid.org.uk/hmrc-announces-temporary-closure-of-its-self-assessment-helpline |

| ↑9 | https://www.theaccountant-online.com/news/icaew-hmrc-service-standard-announcement-signals-new-low/?cf-view |

| ↑10 | https://www.accountingweb.co.uk/tax/hmrc-policy/restrictions-to-hmrcs-helplines-raise-concerns |

| ↑11 | https://committees.parliament.uk/oralevidence/13689/pdf/ Q246+ |

| ↑12 | https://assets.publishing.service.gov.uk/media/5a81e74ae5274a2e8ab56736/HMRC_Annual_Report_and_Accounts_2016-17__print_.pdf R10 para 16. |

| ↑13 | https://www.ft.com/content/ca5716f5-a449-4561-b1d6-d5b9e4dd441d?accessToken=zwAGD50Jx9wYkdPKVxb1pElFYdOx1tW55N1EHQ.MEQCIHuvsTah5AGk9WxjMtKGUdkf9ZOayyTTtQZwJxLKF7FWAiAX9IB9G4EUbR7MUToivKhOssuWX_5c3AvY4MTIVFee1g&sharetype=gift&token=eb3cf07e-b0f3-4c7a-93de-43000e128cb4 |

| ↑14 | https://committees.parliament.uk/oralevidence/14126/pdf/ Q85 – Q90 |

| ↑15 | https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels |

| ↑16 | HMRC’s customer service staff numbers revealed (rsmuk.com) |