HMRC’s Tax Gap increases for 2nd year in a row on like-for-like basis

- Latest HMRC estimate of non-compliance £32bn, or 5.1% of total tax revenues – the same gap as a percentage in 2021.

- This year’s figure includes a £0.7bn revision downwards to compensate for lower compliance activity during Covid. This means that on a like-for-like basis HMRC’s Tax Gap increased for a 2nd year in a row.

- Tax Fraud a minimum of £14.4bn based on the limited data available in the HMRC Tax Gap report. An increase as a percentage on previous years.

- Estimates of error and fraud in the HMRC administered Covid-19 support schemes are not included in the figures.

- HMRC estimate continues to overlook key areas of public concern such as profit shifting by multinationals and offshore tax evasion.

23 June 2022 – George Turner

Summary

HMRC’s Tax Gap, the annual estimate of the amount of tax lost each year in the UK is a matter of huge public interest.

HMRC has been collecting data and making estimates of the Tax Gap since the early 2000s, and has published them every year since 2008. It is the only tax authority in the world that publishes an annual estimate of tax losses for all forms of taxation.

This year’s Tax Gap, covering the 2020-2021 financial year, stands at £32bn, or 5.1% of tax liabilities. This is down from £34.4bn the previous year, which was also 5.1% of tax liabilities.

The amount of the Tax Gap resulting from fraud has increased from 43.7% to 45%, with the Tax Fraud Gap standing at £14.4bn.

This briefing sets out some background to the Tax Gap, how it is calculated and how the presentation of data can be improved.

The UK Tax Gap

In the UK the Tax Gap is defined as “The difference between the amounts of tax that should, in theory, be collected by HMRC, against what is actually collected”.

This is a broad measure of tax non-compliance which covers tax losses arising from a variety of reasons, from innocent mistakes to complex frauds carried out by criminal gangs.

HMRC does not provide a break down of the amount of the Tax Gap that arises from fraud, although some conservative estimates can be made by analysing the HMRC data.

The UK Tax Gap is a net figure, and takes into account ‘compliance yield’ – which is the amount of tax collected though enforcement activity.

The difference between the net and gross Tax Gap is substantial. In previous years, the compliance yield figure is equivalent to 1/3rd of the net Tax Gap.

Estimates on tax losses are notoriously difficult to make. A significant amount of HMRC’s Tax Gap derives from historic data which is projected forward. For example, the amount of corporate tax avoided in the 2021 data comes from the percentage of estimated tax avoided in the previous year (2020), applied to the most recent year’s estimate of total tax liabilities.

The way in which the Tax Gap is constructed therefore means that there will be little change from year to year, with the main driver of a change in the figures coming from changes in the total amount of tax liabilities.

The reason for tax losses

The total amount of the Tax Gap arising from people making mistakes on their tax returns is £3bn. Negligence is the largest component of the Tax Gap – at £6.1bn

HMRC does not provide any estimate of the amount of tax lost to fraud, unlike the Department of Work and Pensions, which analyses benefits underpayments in terms of fraud, claimant error and official error.

Instead, HMRC identify several behaviours leading to non-compliance, which broadly correspond to the way in which HMRC manages their compliance work.

However, it is clear that some of these behaviours arise from fraudulent or dishonest behaviour, specifically “Criminal Attacks – £5.2bn”, “Evasion – £4.8bn”, “Hidden Economy – £3.2bn” and “Avoidance – £1.2bn”.

Taken together, these behaviours account for £14.4bn in tax losses, 45% of the entire Tax Gap. This is a small increase on previous years.

Avoidance is included given the way in which HMRC’s define avoidance. This excludes tax planning and is limited to non-compliance arising from tax schemes that attempt to “exploit” the tax system through “contrived or artificial” transactions. These schemes usually involve fraudulent behaviour at some stage of their execution.

Some categories of behaviour which HMRC use to define the Tax Gap will contain a mixture of honest and dishonest behaviour. For example, Legal Interpretation (£3.7bn) – can include disputes that arise from either honest or dishonest interpretations of tax law on the part of tax lawyers.

This means the figure of £14.4bn for tax fraud will not account for all tax losses arising from fraud. TaxWatch has recommended that HMRC should publish an estimate of all tax losses arising from fraudulent behaviour.

|

£bn |

2021 |

2020 |

2019 |

2018 |

2017 |

|---|---|---|---|---|---|

|

Criminal Attacks |

5.2 |

5.2 |

4.5 |

4.9 |

5.4 |

|

Evasion |

4.8 |

5.5 |

4.6 |

5.3 |

5.3 |

|

Hidden Economy |

3.2 |

3 |

2.6 |

3 |

3.2 |

|

Avoidance |

1.2 |

1.5 |

1.7 |

1.8 |

1.7 |

|

Tax Fraud Gap |

14.4 |

15.2 |

13.4 |

15 |

15.6 |

|

Total Tax Gap1 |

32 |

34.8 |

31 |

35 |

33 |

|

% of Tax Gap resultant from fraud |

45.00% |

43.68% |

43.23% |

42.86% |

47.27% |

1It should be noted that these figures are taken from the reports published at the time, and do not reflect future revisions in the Tax Gap, which can lead to fluctuations in the total Tax Gap.

Covid 19

This year’s figures are the first impacted by Covid-19. During the pandemic, HMRC paused a large amount of its compliance work. Because the Tax Gap is a net figure which includes compliance yield, then this should have led to a significant increase in the Tax Gap figures. However, HMRC made an adjustment to their methodology to change how they accounted for compliance yield. This apportioned the drop in compliance yield to previous years and reduced this year’s Tax Gap by £700m or 0.1% of total tax liabilities. 1See Tax Gap section on Self Assessment – https://www.gov.uk/government/statistics/measuring-tax-gaps/4-tax-gaps-income-tax-national-insurance-contributions-and-capital-gains-tax

This is significant because had this adjustment not been made, the Tax Gap will have increased as a % of total tax liabilities for two years in a row.

The 2020-2021 figures do not include estimates of fraud and error arising from the three coronavirus support schemes which HMRC administered; Coronavirus Job Retention Scheme (CJRS, more commonly known as furlough), Self-Employment Income Support Scheme (SEISS), and Eat Out to Help Out (EOHO).

HMRC’s 2020-2021 annual accounts, published in November 2021, estimated the error and fraud in these three schemes for that year at £5.8bn. How much of this exactly is fraud not yet clear.

If the Tax Gap were to include the drop in compliance yield in line with previously published figures, and the losses to the Covid relief schemes, then the total Tax Gap would be £38.4bn, or 6% of total tax liabilities, an increase of nearly 20% on the previous year’s figures.

Tax Avoidance by Multi-national Corporations

The UK Tax Gap does not estimate the impact of all types of tax avoidance and evasion. HMRC’s definition of avoidance explicitly does not measure the impact of profit shifting by multi-national companies in their Tax Gap methodology. This is a serious problem. Profit shifting is the most high profile form of tax avoidance, the type of avoidance employed by large global businesses like Google, Starbucks, Apple and Nike.

Although it is notoriously difficult to develop an accurate estimate for the impact of profit shifting on the tax take, academic studies found that losses to the UK Treasury due to profit shifting could by up to £20bn a year. HMRC’s figure for non-compliance of all forms by large companies is £0.6bn.

The exclusion of profit shifting from the Tax Gap calculations means that these figures cannot really be considered to be a comprehensive or reliable estimate of tax avoidance in the UK. It is certainly not a measure of tax avoidance that the public would recognise.

Other tax losses

Another area of concern is the potential tax losses arising from offshore bank accounts.

An FOI request from 2021 by Dan Neidle, a tax lawyer, found that HMRC did not have an estimate of the amount of money held in offshore bank accounts by UK tax payers that resulted from tax evasion. 2Dan Neidle, Tax Policy Associates report: UK taxpayers have £570bn in tax haven accounts, and HMRC has no idea how much of this reflects tax evasion, … Continue reading

In total, the data supplied by HMRC showed that UK taxpayers had £570bn held in tax haven bank accounts as of 2019. HMRC’s estimate of the Tax Gap for all types of non-compliance by wealthy taxpayers is £1.2bn.

Another area of concern is the payment of corporate subsidies via the tax system. There is no mention in the Tax Gap of non-compliance in the area of tax reliefs, such as R&D tax credits. The National Audit Office has failed to sign off on HMRC’s accounts for the previous two years because of concerns over R&D tax credits.

Under HMRC’s own estimates, the Treasury lost £336m to fraud and error in the R&D tax credit system. HMRC should clearly state how it deals with corporate benefit payments in its Tax Gap, and whether fraud and error in these programmes are included in their Tax Gap estimate.

HMRC’s interpretation of tax law

The term, “what should be collected” is also problematic as the word “should” is of course open to interpretation. HMRC defines what “should” be collected as – “the tax that would be paid if all individuals and companies complied with both the letter of the law and HMRC’s interpretation of the intention of Parliament in setting the law (referred to as the spirit of the law)”. This is in effect a measure based on how HMRC chooses to apply the law.

This is problematic. It suggests that HMRC can easily reduce the Tax Gap by simply being more lenient in the way it interprets the law.

This puts HMRC in a difficult position with regards to the Tax Gap. If there was demand for HMRC to take a tougher stance on tax avoidance, that in itself would cause an increase in the Tax Gap, leading to a perception that the agency was performing poorly. It means that the way in which the Tax Gap is calculated creates an incentive for HMRC to take a more lenient approach.

Another consequence of this approach is that the Tax Gap does not consider how legislation should be changed to deal with problems with the tax system. Say for example HMRC considers a certain practice to be a form of tax avoidance, but some defect in the law prevents HMRC from pursuing the matter – the classic case of the legal loophole. HMRC would not count the impact of such loopholes in their calculation of the Tax Gap. Indeed, where HMRC has decided that a particular scheme employed by a company or individual is an unlawful act of tax avoidance, but has lost the case in the courts, future users of that scheme will not be included in the Tax Gap.

This is inconsistent with the approach taken with the HMRC compliance yield calculation, which includes estimates of the impact of changes in legislation that HMRC has advised on.

HMRC could look at a broader gap, a tax policy gap, assessing what could be collected if all forms of evasion and avoidance were eliminated and all tax subsidies were abolished. HMRC was advised to put together these estimates by the International Monetary Fund when it last reviewed the HMRC Tax Gap methodology in 2013 – HMRC has not implemented this recommendation.

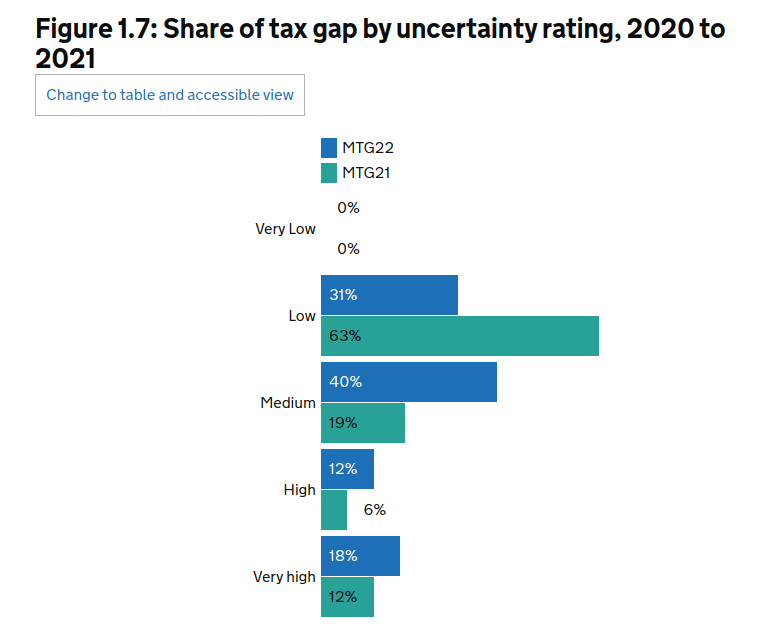

Uncertainty

One significant change in the 2022 Tax Gap edition is the amount of uncertainty in the figures. HMRC categorise their estimate of various tax losses that comprise the Tax Gap by the level of uncertainty in the figures.

In 2022 the amount of the Tax Gap that fell into the “low uncertainty” category halved from 63% to 31%.

The reason for this is the impact of the pandemic on tax collection, which saw VAT payments deferred and more time given for people to pay their tax returns. HMRC say in their figures that they have used historic trends to estimate this year’s figures where data is not available. This would appear to be conservative given the circumstances of the pandemic, where we would expect to see higher levels of tax losses due to insolvency and business failure.

The lowest Tax Gap in the world?

It is frequently stated that the UK has one of the lowest Tax Gaps in the world. This is misleading. It suggests that at the very least there are a number of countries that measure Tax Gaps in a broadly comparable way.

In fact, HMRC themselves say that the UK is the only country in the world that publishes an annual Tax Gap figure that deals with a comprehensive range of direct and indirect taxes.

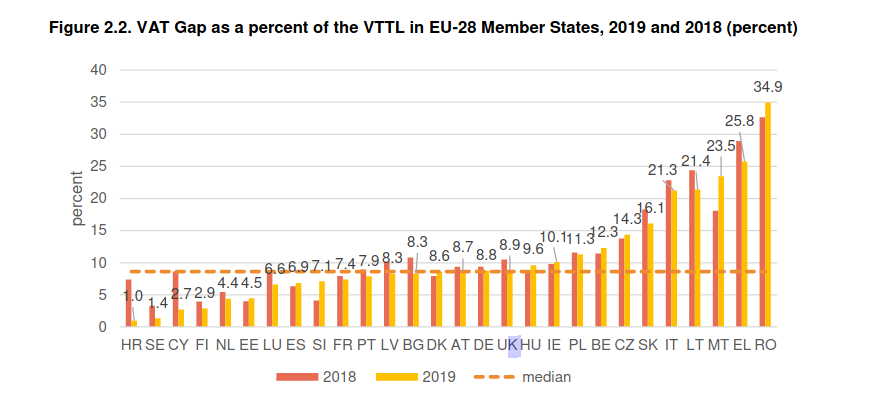

Many countries publish Tax Gaps looking the Tax Gap on specific taxes such as VAT. As the Tax Gap varies considerably between different types of taxes, it is not possible to compare the UK’s broad Tax Gap figure with these estimates. Indeed, VAT is a tax which is particularly targeted by criminal attacks and as such, comparing the Tax Gap across all forms of tax with published VAT gaps in other countries will make it appear that the UK’s Tax Gap is low by international standards. However, when the figures are compared on a like for like basis (i.e. comparing the UK VAT gap with other VAT gaps) the UK does not perform particularly well.

The European Commission regularly assess the VAT gap across all EU states. The latest figures are for 2019, when the UK was still a member of the European Union. This put the UK as mid-table with the 12th highest Tax Gap of all EU states as a percentage of total potential VAT revenues. 3European Commission, The VAT Gap in the EU: 2021 Edition, available from: https://op.europa.eu/en/publication-detail/-/publication/bd27de7e-5323-11ec-91ac-01aa75ed71a1/language-en/

Some countries do publish comprehensive Tax Gap estimates, however, the they use very different methodologies and techniques. For example, the Internal Revenue Service in the US publishes two estimates, the gross Tax Gap which it defines as the difference between true tax liability for a given tax year and the amount that is paid on time. The agency also publishes a net Tax Gap including the amount it will recover after late payments and enforcement action. The study is not published on an annual basis, but retrospectively on a periodical basis. The latest IRS Tax Gap estimate covers the tax years 2011-2013.

Italy publishes a Tax Gap that looks at a broad range of taxes on an annual basis. However, the methodology used differs substantially from the HMRC methodology, making like for like comparisons impossible.

References

| ↑1 | See Tax Gap section on Self Assessment – https://www.gov.uk/government/statistics/measuring-tax-gaps/4-tax-gaps-income-tax-national-insurance-contributions-and-capital-gains-tax |

|---|---|

| ↑2 | Dan Neidle, Tax Policy Associates report: UK taxpayers have £570bn in tax haven accounts, and HMRC has no idea how much of this reflects tax evasion, https://www.taxpolicy.org.uk/2022/05/27/crs-evasion/ |

| ↑3 | European Commission, The VAT Gap in the EU: 2021 Edition, available from: https://op.europa.eu/en/publication-detail/-/publication/bd27de7e-5323-11ec-91ac-01aa75ed71a1/language-en/ |