25th October 2023

Download the report as a PDF (0.6Mb)

Introduction

His Majesty’s Revenue and Customs (HMRC) carries out the vital role of administering and policing the tax system, and its performance is critical to many aspects of the country’s economy and welfare. HMRC collected total tax revenues of £814bn in 2022-231Annual report and accounts 2022-23, HMRC, 17 July 2023, … Continue reading, up almost £83bn (just over 11%) on the previous year and a 34% increase on 2020-21. These amounts are affected by economic activity, inflation, tax rates and other changes to tax legislation alongside HMRC’s compliance activity. HMRC identifies that the growth in income tax and NICs receipts comes from higher NIC rates and strong employee earnings, combined with frozen rate band thresholds and allowances. VAT receipts have also increased due to inflation and higher consumer spending. However, HMRC also points out that there are greater numbers of people falling within the income tax regime, which means that more customers require their support. This, alongside inflation, has driven up the costs of HMRC’s own operations.

This is the second TaxWatch report into the state of tax administration, which reviews HMRC’s performance in a range of areas following the release of HMRC’s Annual Report and Accounts (ARA) for 2022/23.

The data included in this report relate to the core HMRC department, excluding Valuation Office Agency (VOA) and Revenue and Customs Digital Technology Services Ltd (RCDTS Ltd).

HMRC’s current challenges

The last report, in February 2022, mainly contained data up to 2020/21 – the peak of the Covid pandemic and just after the new UK/EU relationship rules came into place on 1 January 2021. Since then, the world has slowly settled down into the ‘new normal’ but still with plenty of economic turmoil.

HMRC was, obviously, heavily impacted by both of those events, which came on top of cuts in resourcing over a number of years. It appears it has a lot of work to do to recover its performance levels in terms of customer service – i.e. services to taxpayers – and customer compliance – i.e. policing compliance by taxpayers.

There have been other major challenges and projects for HMRC over the last couple of years. It is coming to the end of a significant programme to modernise its estate, moving employees to a small number of regional centres in the main UK cities. The closure of smaller offices meant some employees were unable to travel to new offices, resulting in the loss of a number of experienced staff to redundancy.

The biggest current challenge for HMRC is the move towards digital services. This has been identified as the answer to many of its performance issues, as enabling people to comply with their tax obligations using online services is clearly the most efficient way to administer the system. However, while much tax administration is now carried out online, the huge transformation programme required to deal with all of the complexities of the taxation system has been beset by problems and delays. Many of the current customer service performance issues have been blamed on HMRC cutting its in-person levels of support too soon, before the digital services are working and well understood.

A major strand of the programme is Making Tax Digital (MTD). This was introduced for VAT from April 2022, and requires the bulk of VAT-registered businesses to maintain digital records and submit return using software compatible with HMRC systems. This was due to be extended to those above certain income thresholds within Income Tax Self Assessment (ITSA) in April 2024, but has now been delayed until April 2026.

There are also a number of significant ongoing compliance issues for HMRC. The Taxpayer Protection Taskforce, put in place to deal with fraud and error in the Covid-19 support schemes, is now winding down, but TaxWatch have previously identified that moving staff into this team from other compliance roles actually resulted in a lower return on investment for those staff. HMRC is also not expecting to recover significant sums wrongly paid out as part of those schemes. In addition, recent research has led HMRC to believe that fraud and error within Research and Development (R&D) tax credit claims are much higher than previously estimated. There has been a publicly acknowledged step-up in compliance activity in this area, but this has led to concerns amongst advisers that the teams conducting enquiries are not trained or experienced enough to deal with this complex area, which is leading to lengthy delays and inconsistent treatment2R&D relief crackdown deterring genuine claims Institute warns, Chartered Institute of Taxation, 3 July 2023, … Continue reading.

Resourcing

HMRC was created in 2005 by the merger of the Inland Revenue and Her Majesty’s Customs and Excise. HMRC brought together most, though not all, of the functions of both organisations.

Everything HMRC does comes down to resourcing. Ultimately, for HMRC to be able to fulfil its duties, it needs two things: money, and sufficient suitably qualified and experienced staff.

Departmental Budget

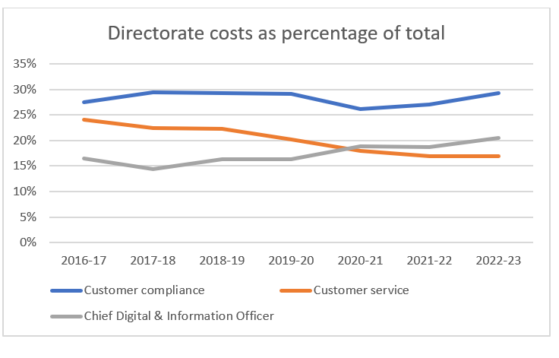

| Running costs | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | 2022-23 |

| Total costs (£m) | 3,931 | 3,868 | 3,929 | 4,316 | 4,741 | 5,139 | 5,460 |

| Of which: | |||||||

| Customer compliance (£m) | 1,079 | 1,139 | 1,149 | 1,255 | 1,242 | 1,392 | 1,603 |

| Customer service (£m) | 945 | 866 | 876 | 870 | 854 | 868 | 928 |

| Chief Digital & Information Officer (£m) | 645 | 557 | 640 | 703 | 893 | 959 | 1,119 |

Total costs of running HMRC have, unsurprisingly, increased over the last few years, not least due to inflation, the additional resources required for Covid support schemes and Brexit. However, customer service costs have not increased significantly over this period, with a large fall between 2016-17 and 2017-18 and actual spending still not returned to 2016-17 levels 6 years later, despite the effects of inflation. The chart shows spending by directorate as a percentage of total departmental spending, which clearly shows the change in focus from spending on customer service to spending on digital services. The consequences of this appear to be reflected in the customer service performance results detailed below.

Compliance costs as a percentage of total spending have remained relatively steady, apart from reductions during the pandemic, likely due to moving compliance staff to deal with the Covid support schemes. However, HMRC is regularly granted one-off funding pots in the budget to deal with particular issues, often around compliance. The flaw in this is that it takes a number of years to train compliance staff, so it is rarely an instant answer to a problem. One-off funding pots also make it difficult to plan long-term staffing. For example, the 2022 Autumn Statement announced a further £79m for additional compliance capacity for 2023-24 to 2027-28, but this a tiny percentage of the total compliance costs across those four years given that it does not make economic sense to recruit and train staff for maximum four-year contracts.

Staff costs as a proportion of total spending have remained relatively stable at around 60% except for a small dip during the pandemic.

Staff numbers

| Average annual Staffing Numbers y/e 31 March | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

| Core department (FTE) | 58,168 | 57,176 | 59,289 | 60,216 | 57,304 | 58,454 | 57,727 | 59,395 | 63,233 |

As reported before, HMRC staff numbers have reduced significantly since the pre-merger days of the Inland Revenue and Customs and Excise. However, total average annual staff within the core HMRC department increased by just under 4,000 in the year to 2022-23, and the department has recruited more people than have left through natural wastage and redundancy over the last few years. This doesn’t tell the whole story, though, as the 2021-22 report and accounts refer to problems with recruitment and retention in relation to issues dealing with customer correspondence3Annual Report and Accounts 2021-22, HMRC, 18 July 2022, … Continue reading.

In recent years there have been regular calls for greater investment in HMRC in relation to both customer service4Open letter on HMRC service levels ahead of the Spring Budget 2023, Tax and accounting professional bodies, 1 March … Continue reading and compliance.

Note: ‘Core department’ excludes Valuation Office Agency and Revenue and Customs Digital Technology Services Ltd

Staff numbers by main directorates

| Staff in post financial year end | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | 2022-23 |

| Corporate Services | 7,861 | 6,827 | 7,913 | 8,530 | 9,454 | 9,287 | 9,700 |

| Customer Compliance | 24,953 | 23,514 | 24,415 | 24,191 | 23,913 | 28,699 | 27,811 |

| Customer Services | 25,643 | 23,965 | 22,504 | 21,887 | 21,220 | 20,205 | 20,195 |

This table shows a significant increase (around 16%) in customer compliance staff across the last two years, despite a small fall in the most recent year to just under 28,000. These numbers were provided by HMRC in response to a Freedom of Information (FOI) request but show some differences from published data in the Annual Return and Accounts (ARA) for 2022-23. The ARA presents the average number of customer compliance staff across the year as increasing from 25,442 to 28,5265Annual report and accounts 2022-23, HMRC, 17 July 2023, … Continue reading. 4,200 staff were said to be recruited into compliance during 2021-22, with these numbers suggesting this was towards the end of the 2021-22 year, but the latest staff in post figures at March 2023 suggest that a number of compliance staff left the compliance team towards the end of 2022-23.

Customer service staff numbers at the year-end are effectively unchanged compared to the previous year but are well below numbers a few years ago following five consecutive years of headcount reductions. This is despite regular performance issues and calls from the professions6Open letter on HMRC service levels ahead of the Spring Budget 2023, Tax and accounting professional bodies, 1 March … Continue reading and politicians7Managing tax compliance following the pandemic, Forty-ninth report of session 2022-23, House of Commons Committee of Public Accounts, 17 April 2023, … Continue reading to increase staffing of customer service due to the impact poor service is having on businesses, individuals and advisers.

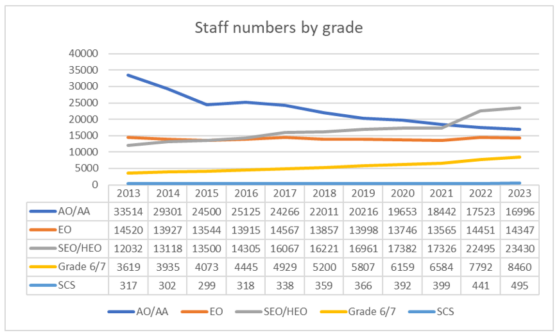

Data on staff grades shows that total staff numbers are roughly back where they were around ten years ago, following significant falls in the mid-2010s. However, the distribution of grades has changed significantly, with numbers at lower administrative grades halving over that time, while numbers at higher operational grades have more than doubled. The fall in administrative grades is not surprising given the move towards automated processing of more and more of the tax system, but customer service performance issues are likely also to be a consequence of this as helplines etc are generally staffed by lower grade staff.

It has been suggested8Civil Service Pay, Institute for Government, 13 February 2023, https://www.instituteforgovernment.org.uk/explainer/civil-service-pay that, as real public sector wages stagnated for many years, the only way staff were able to obtain salary increases was by promotionwhich may partially explain the increase in higher grades as recruitment and retention became an issue. However, it must also be recognised that the tax system continually increases in complexity so likely needs higher-capability staff to deal with that.

Staff engagement

| Staff survey scores | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| Civil service median engagement index | 61% | 62% | 63% | 66% | 66% | 64% |

| HMRC engagement index | 50% | 49% | 49% | 57% | 59% | 59% |

| Selected themes: | ||||||

| Pay and benefits | 24% | 22% | 20% | 23% | 48% | 36% |

| Leadership and managing change | 34% | 39% | 37% | 49% | 52% | 49% |

The Civil Service conducts a staff survey across all departments each year to produce an engagement score based on responses to certain questions regarding how staff feel about working for their employer. These are calculated from scores across a range of themes including ‘pay and benefits’ and ‘leadership and managing change’, for which HMRC has particularly low scores. Staff engagement indicates levels of morale which can impact on both recruitment and retention, and also performance if scores are low. The results for HMRC show a marginally improved engagement score over the last three years from 57% to 59% (2022), although it is still some way below the median civil service score of 64% in 2022. It seems likely that a large part of the increase derives from improved feelings about pay and benefits (up from 23% in 2020 to 48% in 2021, though falling back to 36% in 2022). This probably reflects a significant pay deal struck by HMRC unions in early 20219Members vote to accept 13% pay deal, First Division Association, 1 March 2021, https://www.fda.org.uk/home/Newsandmedia/News/13-pay-deal-for-HMRC-members.aspx following many years of zero or below-inflation pay increases.

Staff development and training

The body of formally qualified staff comes from recruitment and internal training, or recruitment of externally-trained staff. HMRC offers a range of tax professional qualifications, the highest being a degree-level Tax Specialist Programme (TSP) – often seen as similar to the external Chartered Tax Adviser qualification.

On average, just under 200 HMRC staff started the TSP programme in the four years to 2022, but this increased to 283 in 2023. The programme duration has recently been shortened to three years (previously four) unless an extension is granted. There is a considerable attrition rate as only 363 people completed the programme in the three years 2020 to 2022. HMRC has told us they do not collect data on the number of employees who hold a formal tax professional qualification, including external qualifications, TSP and its predecessor equivalents. It is concerning that HMRC does not keep track of the qualification levels of its staff as fully trained and experienced staff are vital for dealing with the most complex aspects of both policy and operational work.

HMRC management categorise a significant number of posts as ‘Tax Professional’. Staff in these roles will have a range of experience and training in tax issues but only a minority of these current postholders will have completed formal qualifications equivalent to TSP (see table below). The number of staff identified by managers as being in a “Tax Profession” role has increased over the last five years from just above 14,000 in January 2019 to over 17,500 in January 2023, though this is down by more than 1,500 from January 2022. It’s likely a large number of these come from the recruitment of 4,200 staff into compliance referred to above, who may need further training whilst in post to fulfil the duties of their roles to best effect.

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

| Staff in a ‘Tax Profession’ role at January | NA | 14,060 | 16,395 | 17,055 | 19,380 | 17,695 |

| TSP recruits starting (September) | 196 | 166 | 187 | 216 | 283 | NA |

| Of which internal HMRC | NA | 124 | 131 | 138 | 160 | NA |

| Number completing by year of starting | 156 | 81 | NA | NA | NA | NA |

| Numbers completing programme by year of completion | NA | NA | 103 | 170 | 90 | 9 |

Note 1: There are still opportunities for people who started in 2019 cohort to complete the programme.

Note 2: There are 4 promotion points with the year so 2023 data is not complete

The accountancy and tax professional bodies have expressed concerns about the lack of knowledge and experience of HMRC staff in some areas of tax compliance, in particular Research and Development10R&D tax relief crackdown deterring genuine claims, Institute warns, Chartered Institute of Taxation, 3 July 2023, … Continue reading.

Interestingly, civil service data show that the median salary for tax professionals – i.e. those in roles identified as Tax Profession – is lower than many other professions within the civil service including Finance, Communications, Statistics, Policy, Economics and Legal11Civil Service statistics: 2022, Statistical tables: Table 45, Cabinet Office, 2 March 2023, https://www.gov.uk/government/statistics/civil-service-statistics-2022, again suggesting that many are not highly qualified staff. There are also questions about how competitive salaries are between the various professions, noting that tax professional roles only exist within HMRC. There is more scope for professionals in other areas to move between Civil Service departments, which could provide upward pressure on salaries that doesn’t apply to staff within HMRC.

There are issues with retention of HMRC-trained staff because they are often courted by private sector tax advisory firms once qualified. These firms can typically offer higher remuneration packages than HMRC’s fixed Civil Service pay scales. Recruitment of tax professionals from the private sector into HMRC is thought to be low, but no data on this is available.

Customer Service

Customer service is a critical part of HMRC’s responsibilities. The easier it is for taxpayers and their advisers to deal with the organisation, the more likely they are to try to – and succeed in – getting things right. Trust in the organisation is also vital to ensure people take their responsibility to pay tax seriously.

This has been a difficult area for HMRC for some years as reduced resources have limited staff availability. This was exacerbated by redeployment during the pandemic. There has been regular publicity about lengthy phone waiting times12Average 27-minute wait on HMRC self-assessment helpline in January, Independent, 25 January 2023, … Continue reading. HMRC has reported a significant number of IT issues affecting its customer service performance in recent years, including a five-day period in December 2022 during which there were no telephone or webchat services13Annual report and accounts 2022-23, HMRC, 17 July 2023, … Continue reading. To illustrate the size of the impact, HMRC reports that they would have expected to handle around 99,000 telephone calls in those five days.

The adviser profession has expressed concerns about the impact poor HMRC customer service is having on them and their clients. All of this is diminishing trust in the organisation14Fair Tax Nation: UK public attitudes to corporate tax conduct, Fair Tax Foundation, June 2023, https://fairtaxmark.net/wp-content/uploads/2023/06/Fair-Tax-Nation-2023-report-final.pdf. Professional bodies are now arguing that this is starting to have an impact on the economy in general as the huge administrative burden affects other activity 15Ministers must resource HMRC properly, says new Institute president, Chartered Institute of Taxation, 30 May 2023, … Continue reading.

It should be noted that there are seasonal bottlenecks for HMRC customer service due to the Self-Assessment return deadline on 31 January each year. Common company accounting periods at 31 December and 31 March also result in bunched return filing deadlines. This creates an additional challenge for HMRC as service requirements vary throughout the year. This is best demonstrated by the much-criticised decision by HMRC to close its Self-Assessment helpline from 12 June to 4 September 202316HMRC to close self assessment helpline for three months, accountingweb, 8 June 2023, https://www.accountingweb.co.uk/tax/hmrc-policy/hmrc-to-close-self-assessment-helpline-for-three-months.

HMRC now interacts with people on many different channels and has been developing new customer service measures which have formal targets from 2022/23. The tables below include comparable data where available, but the new measures will gradually be added into the report as appropriate.

HMRC is also now measuring overall customer satisfaction with different aspects of their services. They are increasingly pushing digital forms of communication with their customers and in recent years have scored an over 80% satisfaction rating for use of digital services. A digital assistant automatically helps taxpayers find the information they need and around 66% of assistant users 17Annual report and accounts 2022-23, HMRC, 17 July 2023, … Continue reading don’t need further help. However, when this does not resolve matters, customers turn to webchat (via a live adviser), phone and post.

However, this raises an important issue around the rapid pace of change within HMRC and, in particular, the move away from direct personal contact and towards the digital provision of services. While laudable in making services as easy to use and cost-efficient as possible, it risks reduced service provision to the digitally excluded18The Guardian view on the digital divide: a growing problem that must be taken seriously, The Guardian, 6 August 2023, … Continue reading who are usually older, poorer and more vulnerable customers. It means these groups are less likely to be able to access the support they need from HMRC to deal with their tax affairs.

Calls and webchat handling

Call numbers had been reducing for some years up to 2020-21, as might be expected with the development of new contact channels. However, there has been an uptick in call numbers in 2021-22 to 35.2m, and then again to 38.3m in 2022-23. Some of this increase probably reflects the increasing number of people having tax obligations, as referenced above. It is likely that additional calls are also created by delays in responding to post (see below) as customers call to chase up a response. Only 72.5% of call attempts were actually responded to on HMRC phone lines in 2022/23, an even lower figure than in the peak Covid year. The average time taken to answer successful calls has also increased substantially in the last few years, with average wait times more than quadrupling in the last six years to 16.24 minutes.

Webchat services (i.e. live online text discussions with an adviser) have much better response rates at over 90% for the last two years, indicating where HMRC is focusing its resources.

| Calls | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | 2022-23 |

| Call Volumes | 60,804,092 | 49,865,940 | 46,745,705 | 42,691,993 | 41,631,930 | 33,308,535 | 35,181,908 | 38,306,681 |

| Average Speed of Answer | 11:54 | 03:54 | 04:28 | 05:14 | 06:39 | 12:04 | 12:22 | 16:24 |

| % of call attempts handled by our Contact Centres | 71.6 | 91.7 | 87.1 | 84.1 | 79.4 | 73.6 | 82.3 | 72.5 |

| % of customers waiting > 10 min to speak to an adviser | – | – | 14.6 | 19.7 | 29.9 | 44.7 | 46.3 | 62.7 |

| Webchat | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | 2022-23 |

| % of webchat adviser attempts handled | – | – | – | – | – | – | 92.9 | 94.7 |

However, in contrast to the HMRC data, a recent poll of members by the Chartered Institute of Taxation (CIOT) showed that only 34% of advisers rated webchat as adequate or better. This compares with 75.6% of all users that HMRC reports as being satisfied or better with the webchat service19CIOT survey into HMRC service levels, Chartered Institute of Taxation, 19 September 2023, https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels. HMRC does not report wait times for access to webchat but CIOT members reported lengthy waits – with nearly half saying they reached an adviser on fewer than 25% of their attempts20CIOT survey into HMRC service levels, Chartered Institute of Taxation, 19 September 2023, https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels.

Post handling

Again, as people move to digital channels the amount of post received by HMRC is on a downward trend, although volumes have picked up again in the last couple of years to nearly 19m items of post in 2022-23. This is roughly around pre-pandemic numbers. This may reflect the greater number of people being brought within the tax system due to frozen thresholds but also problems with getting to speak to someone on the telephone.

Reporting of data about dealing with post now includes data on iforms, i.e. online forms completed by customers, meaning it is not directly comparable with historic data. It is assumed that iforms are simpler to resolve, as they will involve fixed options for responses. Adding these into the statistics for post does appear to have improved the percentage turnaround times (e.g. in 2021-22 39.5% of post only was turned around within 15 days, whereas the combined figure for post and iforms was 45.5%.) The large reduction in rates of post clearance shown in 2021-22 has recovered to some extent in 2022-23, although HMRC is still missing its target to achieve a 15-day turnaround for all post and iform items – it only achieved this in 72.7% of cases. Just under 90% of post and iforms are dealt with within 40 days.

However, the potential problems created by the imposition of targets like these is demonstrated by the fact that HMRC recently set up a task force to deal with post that is more than 12 months old21HMRC responds to postal concerns with new taskforce, AccountancyAge, 11 July 2023, https://www.accountancyage.com/2023/07/11/hmrc-responds-to-postal-concerns-with-new-taskforce/. Once a piece of post is more than 40 days old, dealing with it will not contribute to meeting any targets, so there is a greater incentive to deal with post that is less than 15 or 40 days old. This creates a situation where post can be left undealt with for a staggering 12 months or more.

| Post | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | 2022-23 |

| Post Volumes | 19,802,549 | 20,369,531 | 18,180,451 | 19,029,213 | 17,293,593 | 15,693,910 | 16,259,654 | 18,959,891 |

| Post cleared within 15 working days (%) | 52.2 | 81.0 | 80.7 | 76.6 | 70.3 | 64.4 | 39.5 | – |

| Post including iforms cleared within 15 working days (%) | – | – | – | – | – | – | 45.5 | 72.7 |

| Post cleared within 40 working days (%) | 87.0 | 96.3 | 97.1 | 96.4 | 88.0 | 85.3 | 60.0 | – |

| Post including iforms cleared within 40 working days (%) | – | – | – | – | – | – | 64.1 | 89.4 |

Complaints

HMRC operates a formal two-tier complaints process. Tier 1 is HMRC’s first attempt to resolve a complaint. If a person is not satisfied with the response at Tier 1 they can ask for the complaint to be looked at again, known as a Tier 2 complaint.

After a marked decrease in Tier 1 complaints between 2015-16 to 2019-20, there was a big jump during the pandemic years. There has been a further increase in 2022-23 to a total of over 90,00 complaints, which is probably not surprising given the issues with customer service. It is noticeable that, apart from a drop in 2020-21, over 40% of Tier 2 complaints have been fully or partially upheld over the last ten years suggesting some issues with the Tier 1 complaints process.

| Complaints | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | 2022-23 |

| Tier 1 number of complaints received | 80,391 | 77,279 | 77,410 | 71,638 | 65,625 | 78,542 | 80,216 | 91,217 |

| Tier 1 % fully upheld | 34.0 | 33.0 | 39.0 | 36.0 | 35.5 | 28.9 | 31.9 | 32.0 |

| Tier 1 % partially upheld | 17.0 | 16.0 | 14.0 | 16.0 | 16.9 | 14.5 | 16.4 | 16.0 |

| Tier 2 number of complaints received | 6,186 | 5,339 | 5,006 | 5,209 | 4,431 | 5,802 | 4,914 | 5,871 |

| Tier 2 % fully upheld | 26.0 | 19.0 | 19.0 | 19.0 | 22.4 | 13.4 | 20.3 | 20.2 |

| Tier 2 % partially upheld | 23.0 | 25.0 | 22.0 | 22.0 | 26.4 | 16.0 | 22.9 | 28.1 |

If an individual is not happy with HMRC’s response to a complaint through its internal process they can take it to the independent Adjudicator. Its latest report22The Adjudicator’s Office annual report, 2023, Adjudicator’s Office,22 June 2023, … Continue reading has identified ongoing problems with HMRC’s internal complaints process, with customers being handled by the Customer Service teams being most disadvantaged. In particular, the Adjudicator received a substantial number of premature complaints in 2022-23 – i.e. from people who had not managed to complete the internal complaints process – indicating problems with that process. The report says this arises due to operational resource pressures, but also that the people receiving this poor response are disproportionately vulnerable due to a range of circumstances.

It’s worth noting that organisations like Tax Aid and Tax Help for Older People are charities, part-funded by HMRC, which provide help to poorer and more vulnerable taxpayers in their dealings with HMRC. But this does not replace the need for properly functioning customer services.

Debt balance

Total debt balance and as percentage of overall revenue

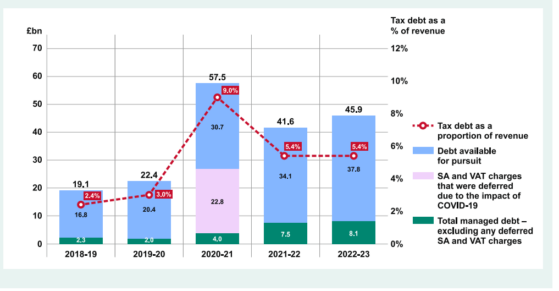

The debt balance is the amount of tax agreed as due and payable but not yet paid to HMRC. Unsurprisingly the debt balance increased substantially during the first year of the pandemic as HMRC reduced pursuit of debts due to the economic turmoil. However, despite a fall in the absolute balance of those debts in 2021-22, they increased again in 2022-23 and HMRC anticipates they will stay high for at least another year. Current cost of living issues are also clearly having an effect. Of the £45.9bn tax debt at the end of 2022-23, £5.7bn is being handled through time-to-pay arrangements, whereby taxpayers pay by instalments. However, these debts continue to accrue interest at a high level (currently 7.75%) making debt clearance even harder. HMRC also identifies that greater tax debts imply there will be a higher value of debts never recovered.

As concerns have been expressed over this level of outstanding debt, HMRC has started to pursue debt more vigorously, including issuing more winding-up petitions in the last year23HMRC winding up petitions push up insolvency figures, Accountancy Daily, 15 September 2023, https://www.accountancydaily.co/hmrc-winding-petitions-push-insolvency-figures.

Compliance

The tax gap is defined by HMRC as the difference between the amount of tax that should, in theory, be paid to HMRC and what is actually paid. By its nature this is difficult to estimate but HMRC produces annual figures estimating the tax gap, focusing on the gap as a percentage of the total theoretical tax due, which varies due to changes in the economy, tax law and inflation. This percentage has been steady at 4.8% in the last two years, amounting to £35.8bn in 2021-22. This figure is calculated after accounting for amounts recovered due to HMRC’s compliance activity (see below).

HMRC’s compliance work aims to keep the tax gap stable24Annual report and accounts 2022-23, HMRC, 17 July 2023, … Continue reading and HMRC carries out its responsibility to police the taxation system in a variety of ways. What is known as upstream compliance is work to encourage voluntary compliance which aims to help taxpayers get things right first time and prevent non-compliance before it happens. This can include education, changes to processes making it easier to comply and other operational activity, eg. the publication of promoters of avoidance schemes to try to prevent further taxpayers using their schemes.

Downstream compliance is the identification and tackling of non-compliance after it has happened. This includes a variety of approaches, such as enquiries into individual taxpayers (known as compliance checks), letters targeted at specific groups of taxpayers and nudges or prompts used to reach a wider audience. Large businesses and very wealthy individuals will have a customer relationship manager who will handle compliance aspects. HMRC takes a risk-based approach to compliance with the aim of policing the tax system across all sectors and sizes, but with a view to making best use of resources to tackle the greatest risks in each area.

Compliance checks

Data for new compliance checks opened by HMRC across all sectors has only been published since 2020-21 and this is not generally broken down by customer sector or type of tax.

| Number of compliance checks | 2019-20 | 2020-21 | 2021-22 | 2022-23 |

| Opened | 361,000 | 247,000 | 265,000 | 299,000 |

| Closed | 351,000 | 248,000 | 256,000 | 280,000 |

The recent NAO review of HMRC’s position on compliance following the pandemic identified that 103,000 fewer compliance checks were closed in 2020-21 than the previous year and 114,000 fewer new cases were opened in that year. These are reductions of 29% and 32% respectively25Managing tax compliance following the pandemic, National Audit Office, 16 December 2022, https://www.nao.org.uk/wp-content/uploads/2022/12/managing-tax-compliance-following-the-pandemic-report.pdf. The latest data shows a steady increase since 2020-21 in the numbers of cases being opened and closed but still approximately 20% lower than the levels indicated by the NAO report for 2019-20 (361,000 opened and 351,000 closed).

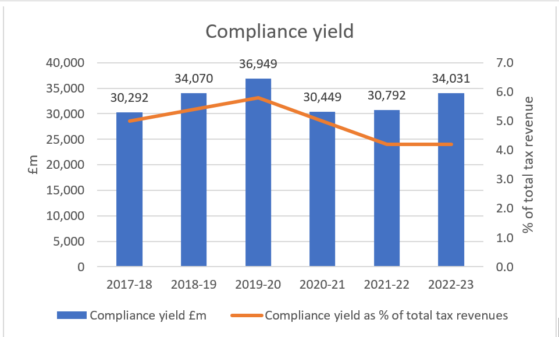

Compliance yield

Compliance yield is the money HMRC recovers or protects through its compliance work. There are a wide range of compliance activities, all measured in different ways and reported under a number of headings. These include amounts arising out of formal enquiries, anticipated future amounts due to changed behaviour and estimates of amounts generated by upstream compliance activity.

This chart shows that returns from compliance activity dropped significantly during the pandemic years, though some of this is potentially due to the reduction in economic activity during those years. In particular, there was a significant reduction in total tax revenue in 2020-21 so, as a proportion of total revenues, the fall in yield in that year was small. Overall, however, the NAO estimates a reduction in compliance yield of around £9bn across the first two years of the pandemic (2020-21 and 2021-22)26Managing tax compliance following the pandemic, National Audit Office, 16 December 2022, https://www.nao.org.uk/wp-content/uploads/2022/12/managing-tax-compliance-following-the-pandemic-report.pdf. This is assumed to be a result of reduced casework activity due to the redeployment of staff to the Covid support schemes. (It should be noted that yield from compliance activity on these schemes is not reported here.)

Compliance yield for 2022-23 has increased since the pandemic years, reaching £34.0bn, up from £30.8bn in 2021-22. However, this was below HMRC’s target of £36bn. This will be affected to some extent by the lower levels of compliance activity during the pandemic years, as some cases can take more than a year to resolve. HMRC also says that providing training and support for the 4,000 additional compliance officers recruited in 2021-22 has taken experienced staff away from compliance work. It takes around four years for new staff to be fully effective in compliance roles, although this is significantly longer for full tax professional staff as described above.

Return on investment

| Compliance RoI per customer segment | 2019-20 | 2020-21 | 2021-22 |

| Individuals | 7.8 | 6.3 | 6.6 |

| Wealthy individuals | 11.6 | 15.8 | 11.4 |

| Small businesses | 15.2 | 11.0 | 13.8 |

| Mid-sized businesses | 18.5 | 11.9 | 13.0 |

| Large businesses | 75.2 | 60.0 | 39.2 |

| Total | 21.8 | 17.4 | 15.5 |

Return on investment in compliance by HMRC has been quoted at around 1:18 in recent years27Treasury Committee, Oral evidence: The work of HMRC, HC 783, House of Commons, 30 November 2022, https://committees.parliament.uk/oralevidence/11972/pdf/ Q158.

This figure varies depending on the customer segment involved, with large business compliance producing very valuable returns, as shown in the table below (n.b. a single large business settlement of £4.2bn in 2019-20 is likely to have distorted figures for that year)28Managing tax compliance following the pandemic, National Audit Office, 16 December 2022, https://www.nao.org.uk/wp-content/uploads/2022/12/managing-tax-compliance-following-the-pandemic-report.pdf). Unfortunately, despite indications that HMRC keeps track of returns on compliance investment29Government response to Thirty-third Report of Session: 2022-23, HM Revenue and Customs, HMRC Performance in 2021-22, The Treasury, 12 April 2023, … Continue reading, the data for 2022-23 have not been included in their latest return and accounts. While the overall return on investment fell to 1:16 in 2021-22, it seems likely that some of this is due to earlier reductions in compliance activity, as yield accruing from casework is often not finalised for more than a year. In fact, complex enquiries can last for many years. Regardless of the recent reductions, HMRC still produces a very good return on investment, which would appear to justify a further increase in compliance resources. However, it is a concern that HMRC appears to have decided to stop publishing this data.

Civil litigation

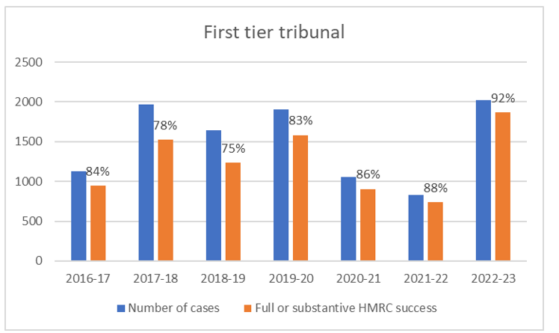

If a tax dispute cannot be settled between HMRC and a taxpayer by agreement, the taxpayer can appeal to an independent tax tribunal. The appeal is first heard at a First-tier Tribunal (FTT). If HMRC or the taxpayer disagrees with the decision of the FTT, a further appeal can be made at the Upper Tribunal, then the High Court, Court of Appeal and finally, the Supreme Court.

The number of cases going to a First-tier Tribunal dropped significantly during the pandemic, when hearings moved to virtual methods (telephone or video), but some hearings have continued to be heard virtually since restrictions lifted. In 2022-23 case numbers at First-tier Tribunal appear to have jumped significantly but these include a group of around 1,000 VAT appeals. If these are excluded, there is still a small increase in cases heard at FTT, but these cases also account for the increase in the success rate at FTT.

It appears substantial progress has been made in tackling the backlog of cases waiting to be heard. There is a substantial number of appeals stood over by agreement between the taxpayer and HMRC to await the outcome of a lead case with similar facts (34,000 in 2022-23 compared with 16,000 in 2021-22). Excluding these, the appeals in progress as of March 2023 were only 5,500, compared with 20,500 the previous March.

HMRC identifies that 49 of the decisions in 2022-23 (42 in 2021-22) relate to tax avoidance issues, with 43 (37 in 2021-22) decided wholly or partially in HMRC’s favour. These decision are said to have protected around £2.3bn in 2022-23, which indicates that many of these are lead cases30Tax tribunal: lead case appeals, HM Courts and Tribunal Services, 20 May 2020, … Continue reading where it has been agreed that the outcome applies to cases with similar facts – often multi-user avoidance arrangements.

Fraud Investigation Service

HMRC’s Fraud Investigation Service (FIS) is the part of the department which deals with the largest and most complex compliance enquiries, and it has separate sections to deal with cases using civil or criminal powers.

In respect of cases where fraud is suspected, HMRC’s policy is to pursue most cases using civil powers rather than criminal. It says: “It’s HMRC’s policy to deal with fraud by use of the cost effective civil fraud investigation procedures under Code of Practice 9 wherever appropriate. Criminal investigation will be reserved for cases where HMRC needs to send a strong deterrent message or where the conduct involved is such that only a criminal sanction is appropriate.”

The criminal arm of FIS conducts criminal investigations into cases identified as the most serious under HMRC’s published criminal investigation policy31HMRC’s criminal investigation policy, HM Revenue and Customs, 13 July 2021, https://www.gov.uk/government/publications/criminal-investigation/hmrc-criminal-investigation-policy.

Criminal cases

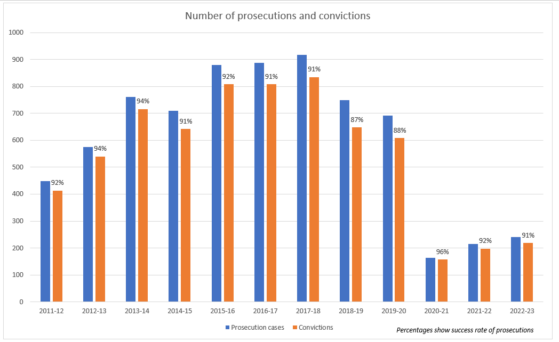

HMRC data on criminal prosecutions show significant reductions in the number of cases in recent years, although this will, to some extent, be due to the pandemic, when some courts were unable to operate for lengthy periods. Numbers have started to increase again slightly over the last couple of years but are still a long way from the highs of the mid-2010s. Positive charging decisions have increased more substantially, but these will take more time to come to court and be reflected in the prosecution statistics. It does, however, suggest that HMRC is moving in the right direction in this area. HMRC has previously reported a focus on more complex and serious cases for prosecution, with a target of 100 such cases set for 2020-21, but it has not reported on this target recently. It now states it has no targets for prosecution volumes but expects numbers to increase in 2022 and 2023 (subject to delays continuing in the courts and the 2022 barristers strike)32Managing tax compliance following the pandemic, National Audit Office, 16 December 2022, … Continue reading. However, the percentage success rate at court is high.

Prosecution is a crucial weapon in HMRC’s armoury for tackling serious offences and creating a deterrent. Reduced activity in this area by HMRC potentially creates the impression that fraudulent behaviour is worth the risk, as the chances of being criminally charged are low. This is particularly demonstrated by activity in relation to professional enablers of evasion, or promoters of avoidance schemes, who are increasingly reported as the cause of a number of taxpayer compliance issues, but who remain largely untouched by HMRC compliance activity. For example, in the five years to March 2022, there were only 66 prosecutions of professional enablers of evasion. Of these, only eight were during the last two years33FOI to HMRC by FT reported here: UK prosecutions of tax evasion enablers drop by 80%, Financial Times, 6 March 2023, https://www.ft.com/content/2b571f7c-6ba5-489f-9450-ac952be9e27d.

HMRC has only reported positive charging decisions (i.e. cases where the Crown Prosecution Service authorises the charging of an individual) in recent years, but numbers have increased from 304 in 2020-21 to 433 in 2022-23. If these figures are compared with the number of cases reaching the courts – 240 in 2022-23, compared with a low of 163 in 2020-21 – this suggests that, even accounting for cases that aren’t ultimately deemed suitable, the stock of cases waiting for court time is almost certainly increasing. This shows that delays in other parts of the public sector are affecting HMRC’s ability to pursue the necessary deterrent effect of convictions for tax fraud.

Civil cases

Complex civil enquiries are carried out by FIS using two Codes of Practice. Code of Practice 934Code of Practice 9, HMRC, 14 June 2023, https://www.gov.uk/government/publications/code-of-practice-9-where-hmrc-suspects-fraud-cop9/code-of-practice-9 (CoP9) is used in cases where fraud is suspected. Code of Practice 835HM Revenue & Customs Fraud Investigation Service – Code of Practice 8, HMRC, February 2018, … Continue reading (CoP8) is used where fraud is not suspected at the outset but is usually used in large, complex cases where there are concerns about offshore aspects, unusual transactions or bespoke avoidance arrangements.

A Freedom of Information (FOI) request to HMRC from a tax adviser in relation to civil cases provided most of the results in the table below, but HMRC has started to publish this data from 2022-23.

| CoP8 | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21* | 2021-22 | 2022-23 |

| Cases opened | 297 | 369 | 258 | 271 | 352 | 176 | 674 |

| Cases closed | 218 | 249 | 380 | 328 | 240 | 279 | 545 |

| Yield recorded | £70,063,729 | £73,691,338 | £118,473,279 | £115,179,253 | £56,011,160 | £70,180,302 | £72,400,000 |

| CoP9 | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21* | 2021-22 | 2022-23 |

| Cases opened | 549 | 486 | 438 | 425 | 363 | 341 | 417 |

| Cases closed | 340 | 375 | 512 | 528 | 540 | 401 | 661 |

| Yield recorded | £161,101,906 | £91,132,829 | £95,829,887 | £121,282,884 | £99,031,451 | £104,343,387 | £89,200,000 |

This shows a jump in the number of CoP9 fraud cases both opened and closed, which is to be welcomed, although the number closed is substantially greater than the number opened. This has been the pattern for a number of years, which suggests there may have been a concerted effort to close older cases which were looking less likely to yield results. This is supported by the reduced average yield from these cases compared with previous years – i.e. an average of £135k per case in 2022-23 vs £260k per case the year before.

A similar pattern is shown for COP8 cases. After a fall in new cases in 2021-22, there is a large jump in 2022-23. A matching large number of settlements indicates attempts to close older, lower-value cases with, again, a much lower average yield – i.e. £133k per case in 2022-23 vs £252k per case in 2021-22.

However, average yield per case demonstrates that these are high value enquiries likely to require significant work to resolve.

HMRC has recently updated Code of Practice 9, said to be as part of a wider push to re-establish CoP9 as its main civil investigation tool for tackling fraud36HMRC publishes revised Code of Practice 9, ICAEW, 16 June 2023, https://www.icaew.com/insights/tax-news/2023/jun-2023/hmrc-publishes-revised-code-of-practice-9 . It will be interesting to see if this results in an increase in the number of new CoP9 enquiries in coming years.

Summary

All of the above demonstrates the difficult time HMRC is still having in recovering from the impact of the pandemic, long-term spending cuts and the switch from personal to digital customer service. There are some positive elements, such as the recruitment of new compliance staff and results in relation to some digital services, such as the HMRC App and online return submission. But repeated criticism of HMRC’s customer service and compliance performance, in both the public and professional media, is reducing trust in the organisation. Possibly more of a concern is the suggestion that HMRC failures are having cost and efficiency impacts on businesses and advisers which ultimately impacts on the wider economy. The organisation has, obviously, been at the centre of some of the most significant political events in the last few years. It now needs to be properly resourced, both financially and in terms of capable staff, to get back to being a department that provides an efficient and effective level of service for all taxpayers and advisers.

References

| ↑1 | Annual report and accounts 2022-23, HMRC, 17 July 2023, https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1172555/HMRC_annual_report_and_accounts_2022_to_2023.pdf p83 |

|---|---|

| ↑2 | R&D relief crackdown deterring genuine claims Institute warns, Chartered Institute of Taxation, 3 July 2023, https://www.tax.org.uk/r-d-tax-relief-crackdown-deterring-genuine-claims-institute-warns |

| ↑3 | Annual Report and Accounts 2021-22, HMRC, 18 July 2022, https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1125182/HMRC_Annual_Report_and_Accounts_2021_to_2022_Print.pdf Fig 15 P50 |

| ↑4 | Open letter on HMRC service levels ahead of the Spring Budget 2023, Tax and accounting professional bodies, 1 March 2023,https://www.att.org.uk/sites/default/files/2023-03/Open-letter-HMRC-service-levels-ahead-of-Spring-Budget-2023.pdf |

| ↑5 | Annual report and accounts 2022-23, HMRC, 17 July 2023, https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1172555/HMRC_annual_report_and_accounts_2022_to_2023.pdf P R24 |

| ↑6 | Open letter on HMRC service levels ahead of the Spring Budget 2023, Tax and accounting professional bodies, 1 March 2023,https://www.att.org.uk/sites/default/files/2023-03/Open-letter-HMRC-service-levels-ahead-of-Spring-Budget-2023.pdf |

| ↑7 | Managing tax compliance following the pandemic, Forty-ninth report of session 2022-23, House of Commons Committee of Public Accounts, 17 April 2023, https://committees.parliament.uk/publications/39357/documents/194186/default/ |

| ↑8 | Civil Service Pay, Institute for Government, 13 February 2023, https://www.instituteforgovernment.org.uk/explainer/civil-service-pay |

| ↑9 | Members vote to accept 13% pay deal, First Division Association, 1 March 2021, https://www.fda.org.uk/home/Newsandmedia/News/13-pay-deal-for-HMRC-members.aspx |

| ↑10 | R&D tax relief crackdown deterring genuine claims, Institute warns, Chartered Institute of Taxation, 3 July 2023, https://www.tax.org.uk/r-d-tax-relief-crackdown-deterring-genuine-claims-institute-warns |

| ↑11 | Civil Service statistics: 2022, Statistical tables: Table 45, Cabinet Office, 2 March 2023, https://www.gov.uk/government/statistics/civil-service-statistics-2022 |

| ↑12 | Average 27-minute wait on HMRC self-assessment helpline in January, Independent, 25 January 2023, https://www.independent.co.uk/money/average-27minute-wait-on-hmrc-selfassessment-helpline-in-january-b2268797.html |

| ↑13 | Annual report and accounts 2022-23, HMRC, 17 July 2023, https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1172555/HMRC_annual_report_and_accounts_2022_to_2023.pdf PR30 |

| ↑14 | Fair Tax Nation: UK public attitudes to corporate tax conduct, Fair Tax Foundation, June 2023, https://fairtaxmark.net/wp-content/uploads/2023/06/Fair-Tax-Nation-2023-report-final.pdf |

| ↑15 | Ministers must resource HMRC properly, says new Institute president, Chartered Institute of Taxation, 30 May 2023, https://www.tax.org.uk/ministers-must-resource-hmrc-properly-says-new-institute-president and Open letter on HMRC service levels ahead of Spring Budget 2023, Various tax and accounting professional bodies, 1 March 2023, https://www.aat.org.uk/prod/s3fs-public/assets/Open-letter-HMRC-service-levels-ahead-of-Spring-Budget-2023.pdf and CIOT survey into HMRC service levels, Chartered Institute of Taxation, 19 September 2023, https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels |

| ↑16 | HMRC to close self assessment helpline for three months, accountingweb, 8 June 2023, https://www.accountingweb.co.uk/tax/hmrc-policy/hmrc-to-close-self-assessment-helpline-for-three-months |

| ↑17 | Annual report and accounts 2022-23, HMRC, 17 July 2023, https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1172555/HMRC_annual_report_and_accounts_2022_to_2023.pdf P34 |

| ↑18 | The Guardian view on the digital divide: a growing problem that must be taken seriously, The Guardian, 6 August 2023, https://www.theguardian.com/commentisfree/2023/aug/06/the-guardian-view-on-the-digital-divide-a-growing-problem-that-must-be-taken-seriously |

| ↑19 | CIOT survey into HMRC service levels, Chartered Institute of Taxation, 19 September 2023, https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels |

| ↑20 | CIOT survey into HMRC service levels, Chartered Institute of Taxation, 19 September 2023, https://www.tax.org.uk/ciot-survey-into-hmrc-s-service-levels |

| ↑21 | HMRC responds to postal concerns with new taskforce, AccountancyAge, 11 July 2023, https://www.accountancyage.com/2023/07/11/hmrc-responds-to-postal-concerns-with-new-taskforce/ |

| ↑22 | The Adjudicator’s Office annual report, 2023, Adjudicator’s Office,22 June 2023, https://www.gov.uk/government/publications/the-adjudicators-office-annual-report-2023/the-adjudicators-office-annual-report-2023 |

| ↑23 | HMRC winding up petitions push up insolvency figures, Accountancy Daily, 15 September 2023, https://www.accountancydaily.co/hmrc-winding-petitions-push-insolvency-figures |

| ↑24 | Annual report and accounts 2022-23, HMRC, 17 July 2023, https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1172555/HMRC_annual_report_and_accounts_2022_to_2023.pdf P13 |

| ↑25 | Managing tax compliance following the pandemic, National Audit Office, 16 December 2022, https://www.nao.org.uk/wp-content/uploads/2022/12/managing-tax-compliance-following-the-pandemic-report.pdf |

| ↑26 | Managing tax compliance following the pandemic, National Audit Office, 16 December 2022, https://www.nao.org.uk/wp-content/uploads/2022/12/managing-tax-compliance-following-the-pandemic-report.pdf |

| ↑27 | Treasury Committee, Oral evidence: The work of HMRC, HC 783, House of Commons, 30 November 2022, https://committees.parliament.uk/oralevidence/11972/pdf/ Q158 |

| ↑28 | Managing tax compliance following the pandemic, National Audit Office, 16 December 2022, https://www.nao.org.uk/wp-content/uploads/2022/12/managing-tax-compliance-following-the-pandemic-report.pdf |

| ↑29 | Government response to Thirty-third Report of Session: 2022-23, HM Revenue and Customs, HMRC Performance in 2021-22, The Treasury, 12 April 2023, https://committees.parliament.uk/publications/38948/documents/191512/default/ Para 3.3 |

| ↑30 | Tax tribunal: lead case appeals, HM Courts and Tribunal Services, 20 May 2020, https://www.gov.uk/guidance/tax-tribunal-lead-case-appeals#:~:text=The%20tribunal%20can%20specify%20lead,the%20lead%20case%20or%20cases |

| ↑31 | HMRC’s criminal investigation policy, HM Revenue and Customs, 13 July 2021, https://www.gov.uk/government/publications/criminal-investigation/hmrc-criminal-investigation-policy |

| ↑32 | Managing tax compliance following the pandemic, National Audit Office, 16 December 2022, https://www.nao.org.uk/wp-content/uploads/2022/12/managing-tax-compliance-following-the-pandemic-report.pdf#page=41 |

| ↑33 | FOI to HMRC by FT reported here: UK prosecutions of tax evasion enablers drop by 80%, Financial Times, 6 March 2023, https://www.ft.com/content/2b571f7c-6ba5-489f-9450-ac952be9e27d |

| ↑34 | Code of Practice 9, HMRC, 14 June 2023, https://www.gov.uk/government/publications/code-of-practice-9-where-hmrc-suspects-fraud-cop9/code-of-practice-9 |

| ↑35 | HM Revenue & Customs Fraud Investigation Service – Code of Practice 8, HMRC, February 2018, https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/684324/COP8_02_18.pdf |

| ↑36 | HMRC publishes revised Code of Practice 9, ICAEW, 16 June 2023, https://www.icaew.com/insights/tax-news/2023/jun-2023/hmrc-publishes-revised-code-of-practice-9 |