The small business tax gap is, on the face of it, the biggest and most urgent problem for UK tax administration.

According to HMRC’s figures, an astonishing £36.7 billion of due taxes went unpaid in 2024/25 by small businesses (those with turnovers under £10 million and typically fewer than 20 employees). That’s an amount of missing tax roughly equivalent to the entire combined budgets of the Home Office and the Department for Science, Innovation and Technology.

HMRC’s estimates of the small business tax gap have increased massively in recent years, and out of sync with the tax gap for other taxpayer categories. In particular, something seems to have happened between 2017-18 and 2021-22 to make the small business gap jump from around 40 percent to about 60 percent of the overall tax gap, and to rise in absolute terms by £23.5 billion over that period.

The problem is, we still have very little idea what that ‘something’ was. We don’t know whether it’s real, or an artefact of measuring the gap differently in recent years, or both. And indeed we have very little idea what kinds of businesses and behaviours make up the small business tax gap to begin with.

In recent years, the debate about the small business tax gap, both inside and outside HMRC, has become partly conflated with anxieties about high street criminality: about the barbers, candy stores and vape shops that are a growing proportion of physical retail in some towns and cities, accused of engaging in a mix of tax evasion, money laundering, counterfeit goods and immigration crime.

In this first of our ‘Tax Gap 2026’ series of posts, we take a look at the evidence about what makes up the small business gap, and what might be driving it upwards. We find that it’s not necessarily the picture of dodgy vape shops and mysteriously under-employed barbers that dominates headlines and policy initiatives.

What taxes and behaviours make up the small business gap?

We can see that Corporation Tax accounts for about half the small business tax gap, and around 40 percent of its dramatic increase since 2017-18. Incredibly, HMRC believes that over half of all small businesses now submit incorrect corporation tax returns, with over a third understating their liabilities by more than £1000.

These statistics suggest extraordinary levels of non-compliance. But they don’t really tell us who are the main culprits, or what they’re doing wrong. ‘Small businesses’ are a hugely heterogenous group: around 5.1 million entities (nine in ten British businesses), ranging from single-person nano-businesses to companies with multi-million-pound turnovers. And profit taxes can be evaded in lots of different ways. Is it cash-in-hand service providers? Retail businesses hiding takings? Illegal and invisible trading? Or something else entirely?

One of the main reasons we don’t know is that HMRC can’t accurately break down the small business tax gap by behaviour. For the tax gap as a whole, HMRC provides estimates for the proportion attributable to eight behavioural causes of tax non-compliance: from criminal attacks on the tax system, to unintentional mistakes. But sub-categories of the overall tax gap — which still represent tens of billions of pounds of missing tax in some cases – are not broken down in the same way.

The reason that HMRC can’t provide this causal split for small businesses specifically – which is absolutely essential for understanding what is going wrong, and thus how to tackle it – is simply because the sample of tax returns that HMRC uses to estimate it is in fact extremely small. Deep in the methodological annexes of HMRC’s publication, we can see that the corporation tax component of the small business tax gap, accounting for about half of the total figure, is based on a random audit of just 337 businesses’ tax returns. That’s 337 out of around 5.1 million small businesses – a sample size of 0.007 percent. And those tax returns where non-compliance is actually detected will be a smaller subset of those 337 sampled returns.

In other words: this giant estimate of over £17 billion of corporation tax going unpaid is based at best on a couple of hundred tax returns.

Just getting one or two more non-compliant tax returns in the small business sample, by chance, will change the overall small business gap by several percentage points. Accordingly, the upper and lower bounds of HMRC’s estimate for the small business corporation tax gap, for instance, range from £9 to £23 billion – a potential variation which is itself about the size of the entire budget of the British Army.

As a result, the small business corporation tax gap is given an uncertainty rating of “high”, primarily because the uncertainty of its data is rated “very high”. To put this into context: “very high” data uncertainty means that HMRC assesses that in estimating the small business corporation tax gap, there is either “no suitable data” or “what is available is not well understood and is of low quality.”

That’s a remarkable situation of non-knowledge to be in, for a statistic ostensibly saying that a sum bigger than the budget of the Ministry of Justice – nearly half of the corporation tax of 90 percent of British businesses – is going unpaid every year.

HMRC is proud of it tax gap statistics, and understandably so. Heralding this year’s release, HMRC’s policy director-general said:

HMRC is internationally recognised as a leader in estimating tax gaps, and is the only revenue authority in the world that measures and publishes such a comprehensive tax gap every year. This makes the UK’s tax gap series one of the most developed and transparent internationally.

HMRC’s tax gap statistics are indeed detailed, extensive, and annual. But they’re not always world-leading in the size and reliability of the evidence base underlying the different figures. As the LSE/Warwick University’s Centre for the Study of Taxation (CenTax) pointed out earlier this week:

In 2023 the IMF reviewed how different countries estimate the small business Corporation Tax gap, and the UK came out at the bottom of the comparison set on sampling rate. Canada uses a sample of 4,500 audits to estimate its tax gap, more than ten times the UK sample. The smallest documented sample size outside the UK was for Denmark, which used a sample of 350 audits, but for a business population that is 10 times smaller than the UK’s. While other countries have around 100 audits per 100,000 of business population, the equivalent figure for the UK is 17.

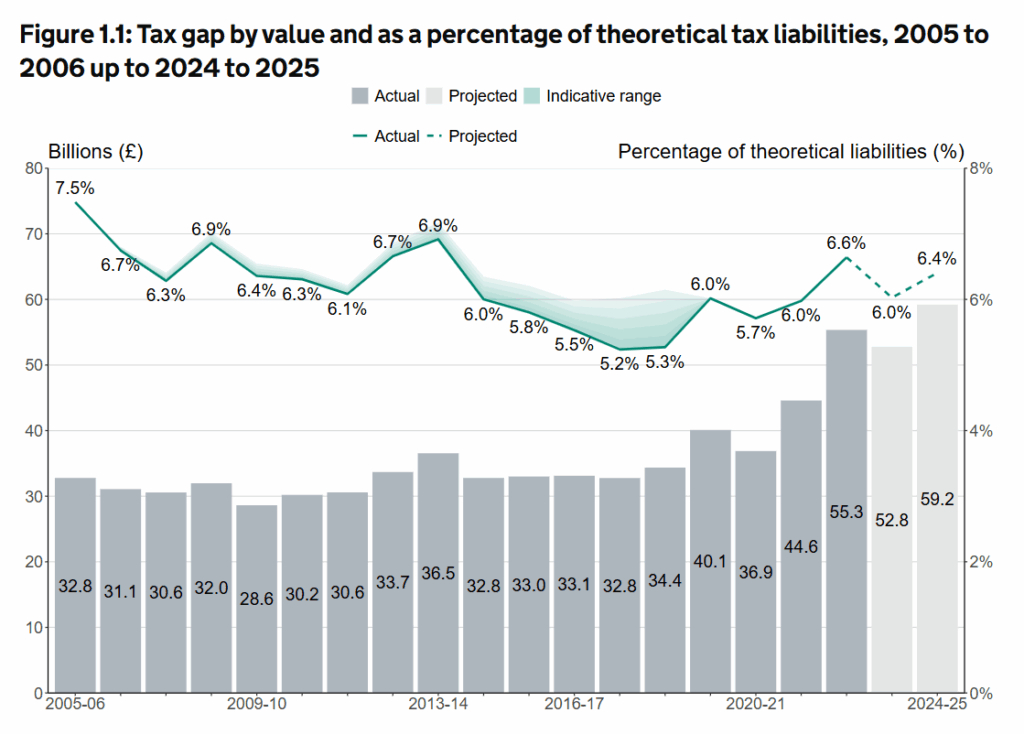

That tiny sample size, on which HMRC has built the huge edifice of the small business tax gap, means that we can’t be sure about either the amount or the overall trend of the tax gap. Indeed, in seeking this week to downplay the fact that the UK’s overall tax gap seems to be increasing significantly, HMRC’s director-general for policy suggested that in fact changes in how the small business tax gap is measured could make the entire rising trend of the nation’s tax gap disappear:

Changes in methodology, particularly improvements in measuring non-compliance among small businesses, mean that earlier estimates are likely to have understated the true level of the tax gap. This also means that some of the apparent increase reflects better measurement, rather than a genuine deterioration in compliance. HMRC has published indicative ranges to indicate how historical estimates may change once methodological improvements are fully incorporated, which is likely next year. Taking this into account suggests that the tax gap has likely been broadly stable over the last few years as a percentage of receipts.

(There’s no detailed explanation about these future ‘methodological improvements’, and indeed, HMRC’s own publications suggest that there has already been significant effort to make earlier years of the small business tax gap a consistent time series with later years: including adjustments to align former SME customer classifications with the current small businesses customer group, and changes in the ‘non-detection’ multiplier applied to earlier years. So it’s unclear where further changes are coming from).

Green shading: unspecified ‘indicative ranges’ added to this year’s tax gap figures, which make apparent recent rises in the tax gap disappear (Source: HMRC)

Nonetheless this ‘high uncertainty’ estimate is now driving HMRC’s resource choices. It’s spending £750 million on small business compliance (and rising). The statistics are also an impetus behind a raft of other initiatives, including a 350-strong new team of HMRC criminal investigators, announced in last November’s budget, to carry out

targeted criminal interventions to tackle the most serious fraud and evasion by small businesses.

Half of those 350 new investigators, the Exchequer Secretary Dan Tomlinson recently announced, are being dedicated to “high street harms”: government shorthand for what Tomlinson called

vape shops, barbers, souvenir shops, candy stores and convenience stores as fronts for money laundering and tax crime.

Exchequer Secretary Dan Tomlinson joins an HMRC raid on a high street vape shop, June 2026 (Instagram: HMRC)

Are these the right interventions to tackle the small business tax gap?

Which brings us to the importance of figuring out what the small business gap actually is.

As we’ve seen, HMRC’s official statistics can’t reliably slice the small business gap by behaviour. It seems likely that high street tax evasion is indeed a significant part of the problem. The ‘high street harms unit’ is unlikely to be money wasted.

But the figure’s high uncertainty also means that there could be new forms of non-compliance within the tax gap going under-addressed,: online sellers faking UK company registrations for VAT purposes, for example, which some argue is potentially a nine-figure tax evasion problem; criminal spoofing of e-payment account ownership; and much more.

Right now we can’t know for sure. But in fact we do have some clues. HMRC officials have said in public fora that they believe that perhaps a third of the gap is small businesses’ “failure to take reasonable care” in their tax returns and tax accounting, and another significant portion is “error”. (These are also behavioural categories that, as the graph above shows, have increased within the overall tax gap estimates more than any others).

This is not vape smuggling or till sales suppression. It’s small businesses getting their tax returns wrong, either unwittingly or carelessly. Such negligence can be a failure of legal obligations and may attract penalties, but it’s not the same as, for example, deliberately hiding income.

One other statistic puts this slice of the small business gap in context. Over two-thirds (68%) of businesses file their tax returns via an agent: an accountant, tax adviser or similar professional. That figure drops to 58% for ‘nano-businesses’ (those with no-employees). Nonetheless we can assume that somewhere between 60 and 70 percent of small businesses use a professional to prepare their tax return.

If it’s true, as HMRC estimates, that over half of small businesses’ tax returns are understating their income, over a third of them by £1000 or more; and if it’s true that perhaps a third to a half of the small business tax gap is due to small businesses messing up their tax returns, whether honestly or negligently; then a substantial slice, at least, of this £37 billion gap must be due to the errors and carelessness – or the failure to correct errors and carelessness – of the professionals that are preparing small businesses’ tax returns.

The UK is unusual in having an entirely unregulated tax advice industry. Anyone can set themselves up as a tax adviser, without any qualifications at all, and without any regulatory oversight. It wasn’t until this year that HMRC introduced some basic fitness tests for those registering to file tax returns on behalf of clients with HMRC, against vociferous opposition from the various professional bodies that represent tax and accountancy professionals.

Perhaps all the errors and carelessness being made or overlooked by tax professionals in small business tax returns are down to the 35% of tax agents that are not affiliated to professional bodies (which do have internal professional standards and internal disciplinary processes, though TaxWatch’s experience of testing the latter has been decidedly mixed).

Nonetheless if HMRC’s estimates are to be believed, such errors and carelessness seems to be amongst the largest sources of unpaid tax in the entire UK tax system. The professional bodies need to answer the question: what are they doing to help reduce the potentially enormous problem of errors and carelessness in professionally-prepared small business tax returns?

And if the problem doesn’t lie with their own members, what is their response (other than their historical blanket opposition) to the evident need for regulation of some kind for the whole profession, both affiliated and unaffiliated?

What gets measured gets done – so we need to measure it right

At TaxWatch we often argue for the government to measure problems in the UK tax system – such as the offshore tax gap, which we’ll write about next week. We think this is important because if we don’t know how big a problem is, there’s rarely the institutional or political impetus to tackle it.

In the case of the small business tax gap we have a different issue. We have a prominent, annual, public measurement of a problem, driving policy, but without any clarity at all as to what kinds of taxpayers or behaviours the problem actually involves.

Government is as vulnerable as civil society tax campaigners to the seduction of big numbers and killer facts (though government tends to get less flack for it). If the small business tax gap is really eating up as much tax revenue as the cost of the UK’s courts service, then we urgently need to know what it looks like. The cost/benefit of significantly expanding the size of the tax return sample underlying it, and segmenting the estimate by different types of business and behaviour, is unarguable. (Or if the capacity doesn’t exist internally, why not anonymise several thousand randomly-selected returns and let the CenTax specialists conduct a detailed analysis?)

In the meantime we need to take seriously the possibility that much of the small business gap, however large it is, may not be criminal vape shops and people-smuggling barbers, but something rather less dramatic: businesses getting their returns wrong and accountants doing a bad job at helping them.

If an expanded analysis of the small business tax gap confirms this, then that points to two important ways to tackle the problem.

First, HMRC needs to redouble its efforts to make it easier and simpler for the smallest businesses to file their returns and get them right. The experiences of other countries could be important – from partly pre-populated returns which are prevalent in countries like Norway, to simplifying national insurance, and changing cliff-edge thresholds like VAT registration.

And second, the professions that have long resisted mandatory standards and regulation in the tax advice market need to come up with a plan for how to reduce the contribution of tax professionals – whether affiliated or unaffiliated – to errors and carelessness.

None of this is as exciting as the Exchequer Secretary on Instagram raiding a vape shop in a high-vis vest. But billions of pounds of public money potentially rests on getting it right.