11th February 2022

11th February 2022

Introduction

This is the first of what is to become an annual TaxWatch report on the state of tax administration in the UK.

Her Majesty’s Revenue and Customs carry out a vital role in administering and enforcing the tax system, and with limited resources. The aim of this report is is to provide an independent analysis of the performance of the government in carrying out that function.

The United Kingdom left the European Union at the end of January 2021, just as Covid-19 was beginning to spread around the world. Brexit saw the UK leave the EU Customs Union, the Single Market, and the VAT area. This has required an entire new system of customs arrangements for the UK, necessitating at least £1bn in investment.1 With the UK Government phasing in border controls on imported goods over 2021 and 2022, the burden is only increasing as time goes on.

Shortly after leaving the EU, in response to the pandemic the UK entered a lockdown, with all but essential workers either furloughed or told to work from home. HMRC officers had to adapt to home work, all while the courts system was placed on a temporary hiatus, causing a significant backlog.

HMRC was tasked with rapidly implementing large scale coronavirus support schemes, supporting incomes as well as businesses. These schemes, while drawn up and administered quickly in order to protect jobs while the country ground to a halt, unfortunately have seen wide scale abuse costing billions of pounds.

The timings of Brexit coupled with the pandemic has resulted in tax administration in the UK facing a difficult task without equal in modern times, causing a huge amount of stress on the system. For that reason, HMRC’s performance over the last year inevitably looks poor.

However, our concern is that after more than a decade of cuts, and with performance already dropping on previous years, the impact of the stress of the last year could cause long term damage to the tax administration if government does not invest significantly more funds in tackling non-compliance and improving customer service.

Sources

Data used in this report is from a variety of sources. A lot of the information stems from publicly available HMRC reporting, including the department’s annual reports and tax gap papers. Other information is from Freedom Of Information requests, either sent by us, or available due to other organisations publishing them.

Elements of this report take up issues which TaxWatch has previously reported on. In the three years since TaxWatch was first established, we have published close to 100 briefings, blog posts, and reports. This paper allows us to take stock of past research, and to put it into context to provide an overarching view of the state of tax administration today.

While this report does not cover the entirety of tax administration, we believe it does highlight several key issues. It is our intent that this briefing will grow year on year, and we welcome any and all feedback.

TaxWatch, February 2022

The Tax Gap

The Tax Gap, the annual estimate of the amount of tax lost to avoidance, evasion and criminal activity in the UK has become a matter of huge public interest in recent years.

In the UK the Tax Gap is defined as “The difference between the amounts of tax that should, in theory, be collected by HMRC, against what is actually collected”. The UK Tax Gap is a net figure, and takes into account ‘compliance yield’ – which is the amount of tax collected though enforcement activity. The difference between the net and gross tax gap is substantial.

The UK Tax Gap does not estimate the impact of all types of tax avoidance and evasion. HMRC explicitly does not measure the impact of profit shifting by multinational companies in their tax gap methodology. This is a serious problem. Profit shifting is the most high profile form of tax avoidance.

Profit shifting is thought to cost the UK billions of pounds in lost revenue a year, and the exclusion of it from the Tax Gap calculations means that these figures cannot really be considered to be a comprehensive or reliable estimate of tax avoidance in the UK.

HMRC attribute all non-compliance to eight behavioural categories: criminal attacks; evasion; hidden economy; avoidance; legal interpretation; non-payment; failure to take reasonable care; and error.

In our analysis of the Tax Gap, we have proposed an alternative categorisation of non-compliance based on the three behavioural categories defined in law: fraud, negligence, and honesty (which includes honest mistakes).2

Our analysis of the definitions underlying HMRC’s behaviours finds that several arise from from fraudulent behaviour, specifically “Criminal Attacks”, “Evasion”, “Hidden Economy” and “Avoidance”. Taken together, these behaviours accounted for £15.2bn in tax losses in 2019-20, 43% of the entire Tax Gap.

While this number as a percentage of the overall Tax Gap does appear to have lowered recently from close to 50% throughout 2016-18, it should be noted that fraud in relation to Covid-support schemes is not included.

Factoring in Covid-related fraud, along with profit shifting, means that in reality the amount of tax lost to fraud will be significantly more, and an estimate of at least £20bn would not be unreasonable.

|

2015-16 |

2016-17 |

2017-18 |

2018-19 |

2019-20 |

|

|

Tax Gap |

£33,000,000,000 |

£32,000,000,000 |

£31,000,000,000 |

£31,000,000,000 |

£35,000,000,000 |

|

Criminal Attacks |

£5,100,000,000 |

£5,400,000,000 |

£4,900,000,000 |

£4,500,000,000 |

£5,200,000,000 |

|

Evasion |

£5,200,000,000 |

£5,300,000,000 |

£5,300,000,000 |

£4,600,000,000 |

£5,500,000,000 |

|

Hidden Economy |

£3,500,000,000 |

£3,200,000,000 |

£3,000,000,000 |

£2,600,000,000 |

£3,000,000,000 |

|

Avoidance |

£1,700,000,000 |

£1,700,000,000 |

£1,800,000,000 |

£1,700,000,000 |

£1,500,000,000 |

|

Total Fraud |

£15,500,000,000 |

£15,600,000,000 |

£15,000,000,000 |

£13,400,000,000 |

£15,200,000,000 |

|

Percentage Fraud |

46.97% |

48.75% |

48.39% |

43.23% |

43.43% |

Resourcing

Her Majesty’s Revenue and Customs (HMRC) was created in 2005 by the merger of the Inland Revenue and Her Majesty’s Customs and Excise. HMRC brought together most, though not all, of the functions of both organisations.

Everything HMRC does comes down to resourcing. Ultimately, for HMRC to be able to do its job, it needs two things, money and personnel.

Staff

HMRC’s staffing numbers are down 40% since the department was created

In 2003–04, prior to the merger, there were some 77,300 staff in the Inland Revenue and some 22,400 in Customs and Excise,3 for a combined total of 99,700 full time equivalent staff. Upon formation, The Treasury stated that there would be a net reduction of 10,500 posts.4

What we have actually seen just under a 40% deduction in staff numbers. In 2020-21, the headcount stands at 57,727 for the ‘core department’, and 61,867 for total staff – a number smaller than 2019-20, despite the extra burdens placed on HMRC as a result of both Britain’s exit from the European Union, and the Covid-19 pandemic. The head of HMRC, Jim Harra, has recently stated that he could “always do with more” staff.5 We agree.

The number of staff employed by HMRC has fluctuated since 2014-15, with 2015-16 seeing the lowest number at 60,914, and 2017-18 the highest at 64,228.

|

Staffing Numbers |

|||||||

|

2014-15 |

2015-16 |

2016-17 |

2017-18 |

2018-19 |

2019-20 |

2020-21 |

|

|

Core department |

58,168 |

57,176 |

59,289 |

60,216 |

57,304 |

58,454 |

57,727 |

|

Total Staff |

61,588 |

60,914 |

63,074 |

64,228 |

61,456 |

62,642 |

61,867 |

|

Notes |

‘Total Staff’ includes ‘core department’, ‘Valuation Office Agency’, and ‘Revenue and Customs Digital Technology Services Limited’. |

||||||

HMRC provided us with a breakdown of HMRC staff by department for the past five years. The below includes Customer Compliance, Customer Services, Transformation, and Corporate Services. All figures are Full Time Equivalent (FTE).

|

2016-17 |

2017-18 |

2018-19 |

2019-20 |

2020-21 |

|

|

Corporate Services |

7,861 |

6,827 |

7,913 |

8,530 |

9,454 |

|

Customer Compliance |

24,953 |

23,514 |

24,415 |

24,191 |

23,913 |

|

Customer Services |

25,643 |

23,965 |

22,504 |

21,887 |

21,220 |

The cost of staff, which includes wages and salaries, social security, and pensions, has increased steadily since 2014-15. The difference over the seven year period to 2020-21 represents a 27% increase.

|

Staff Costs (£m) |

|||||||

|

2014-15 |

2015-16 |

2016-17 |

2017-18 |

2018-19 |

2019-20 |

2020-21 |

|

|

Total net costs |

2,178 |

2,259 |

2,418 |

2,456 |

2,417 |

2,654 |

2,773 |

HMRC is seeing an increase in staff leaving. 2020-21 saw 2,118 members of staff leave the organisation, an increase on the 1,298 of 2019-20, which was again an increase on the 1,037 of 2018-19. This is a 104% increase in departures over a three year period. While some of this will be to do with the reorganisation of HMRC seeing a move into regional offices, morale will also partially be to blame.

The 2020 Civil Service People Survey saw an ‘Engagement Index’ of 57% at HMRC, notably lower than the 66% Civil Service Median Benchmark, with only 23% happy with pay and benefits, and 49% with ‘leadership and managing change’.6

Staff dissatisfaction can increase staff turnover, and with it the accompanying recruitment and training costs, but it can also reduce performance amongst the unmotivated workforce that remains.

Budget

Budget increases are going to Brexit. Spending on compliance has fallen

In the Autumn 2020 Budget, Chancellor Rishi Sunak stated that HMRC is set to see a “£0.9 billion cash increase over the Parliament to £5.2 billion in 2024-25”.

Spending Review 2020 revealed that £1bn would be going to HMRC “to reform and enhance the UK customs system after the end of the transition period, including investment in vital physical and IT infrastructure and additional support for UK traders”.7 So while the £0.9bn cash increase sounds impressive, it’s worth bearing in mind that all of this (and more) will go towards dealing with the additional complexities surrounding the UK’s departure from the European Union.

HMRC’s annual report 2020-21 does show an increase in compliance related expenditure for every year apart from 2020-21, where spending then dips. Taking into consideration inflation and increases in staffing costs, it begs the question as to how much of this is really increasing capacity.

Indeed, as can be seen from the table above, there are around 1000 fewer staff working in customer compliance as there was in 2016.

|

Expenditure (£m) |

|||||||

|

2014-15 |

2015-16 |

2016-17 |

2017-18 |

2018-19 |

2019-20 |

2020-21 |

|

|

Customer Compliance (gross) |

n/a |

n/a |

1,079 |

1,139 |

1,149 |

1,255 |

1,242 |

|

Enforcement and Compliance (gross) |

1,018 |

1,056 |

n/a |

n/a |

n/a |

n/a |

n/a |

|

Gross Expenditure |

3,617 |

3,792 |

4,281 |

3,901 |

3,905 |

4,316 |

4,741 |

|

Income |

149 |

217 |

429 |

206 |

226 |

371 |

439 |

|

Net Expenditure |

3,468 |

3,576 |

3,853 |

3,695 |

3,704 |

3,945 |

4,302 |

|

Notes |

‘Customer Compliance’ and ‘Enforcement and Compliance’ are thought to be the same thing, and that HMRC’s naming conventions changed between the 2015-16 year and the 2016-17 year. |

||||||

In the latest budget and spending review, more investment in compliance was announced, including an additional £292m over the next three years to tackle the tax gap.

Extra spending on compliance will not, however, lead to more in tax being collected until 2023-24. The March 2021 budget estimated that less tax would be collected in 2021-22 and 2022-23, despite the extra investment in compliance. One reason give for this is the “impacts on compliance yield reflecting reprioritisation (including to respond to COVID19).”8

Compliance

Criminal investigations fell by 50% during the pandemic. HMRC management seem to not know how many audits of tax returns are being carried out.

Audits and Compliance Checks

In September we sent multiple Freedom of Information requests to HMRC regarding audits and compliance checks. An audit involves a tax official undertaking a review of a return to ensure that what has been entered onto it is in fact correct.

HMRC’s latest tax gap document revealed that £7bn of the tax gap is from self assessment. Research by Dr Arun Advani of the University of Warwick shows that while audits cost on average £2,500, a targeted audit bring in around £10,000-15,000 when changes in future behaviour are factored in.9 This is a return of between 4:1 and 6:1.

|

Tax |

Type |

Component |

Percentage tax gap |

Point estimate (£ billion) |

|

Income Tax, NICs, Capital Gains Tax |

Self Assessment |

Non-business taxpayers |

8.00% |

1.6 |

|

Income Tax, NICs, Capital Gains Tax |

Self Assessment |

Business taxpayers |

22.50% |

4.3 |

|

Income Tax, NICs, Capital Gains Tax |

Self Assessment |

Large partnerships |

8.80% |

1.1 |

|

Income Tax, NICs, Capital Gains Tax |

Total Self Assessment |

Total Self Assessment |

13.40% |

7 |

Given the cost benefit of audits, it would seem logical that HMRC should be aware of how many are conducted. When asked how many audits or compliance checks are carried out into ‘High Net Worth’ or ‘Affluent’ (both HMRC definitions) individuals, HMRC confirmed that while they do hold that information, it would take over 3½ working days to compile the data. When asked more generally how many audits or compliance checks HMRC do, we were given the same answer.

What this tells us is that nobody in HMRC is actually aware of the amount of audits or compliance checks they are doing, and that senior management have not asked for this reviewed in the past. If they had done, this information would be readily available.

Civil Fraud investigations

It is HMRC’s policy that they will not prosecute most cases of tax fraud as a criminal offence, instead having a preference to pursue civil claims. This is clearly stated in HMRC’s criminal investigation policy which states the following:

“It’s HMRC’s policy to deal with fraud by use of the cost effective civil fraud investigation procedures under Code of Practice 9 wherever appropriate. Criminal investigation will be reserved for cases where HMRC needs to send a strong deterrent message or where the conduct involved is such that only a criminal sanction is appropriate”10

COP8 and COP9 are the two main methods of civil investigations carried out by HMRC, with both conduced by the Fraud Investigation Service (FIS).

A COP8 investigation is conducted when HMRC suspect tax avoidance, and is used to recover tax, interest, and penalties due. They are not undertaken with a view to a criminal prosecution, though if HMRC suspect fraud it may then be investigated under COP9, or with a view to a criminal prosecution. A COP9 involves inviting a taxpayer to formally admit that they have been complicit in tax fraud. If the taxpayer accepts and cooperates with HMRC, they receive immunity from criminal prosecution.11

A Freedom of Information request from an accountancy firm revealed the number of investigations carried out by HMRC under COP8 and 9.

|

CoP8 |

2016-17 |

2017-18 |

2018-19 |

2019-20 |

2020-21 |

|

Cases opened |

297 |

369 |

258 |

271 |

352 |

|

Cases closed |

218 |

249 |

380 |

328 |

240 |

|

Yield recorded |

£70,063,729.00 |

£73,691,338.00 |

£118,473,279.00 |

£115,179,253.00 |

£56,011,160.00 |

|

CoP9 |

2016-17 |

2017-18 |

2018-19 |

2019-20 |

2020-21 |

|

Cases opened |

549 |

486 |

438 |

425 |

363 |

|

Cases closed |

340 |

375 |

512 |

528 |

540 |

|

Yield recorded |

£161,101,906.00 |

£91,132,829.00 |

£95,829,887.00 |

£121,282,884.00 |

£99,031,451.00 |

The number of COP9 cases has declined steadily year on year for the past five years, with COP8 also trending downwards. This is not due to HMRC pursuing more criminal investigations (See Criminal Investigations below). The fact is that there is just an overall downward trend in compliance investigations, regardless of how they are pursued.

Litigation and appeals

If a tax dispute cannot be settled between HMRC and the taxpayer by agreement, the taxpayer can appeal to an independent tax tribunal. The appeal is first heard at a First-tier Tribunal. If HMRC or the taxpayer disagrees with the decision of the FTT, a further appeal can be made at the Upper Tribunal, then the High Court, Court of Appeal, and finally the Supreme Court.

The reason for the drop in hearings in 2020-21 is a result of the pandemic, with the FTT cancelling face to face hearings. HMRC did not publish data on this issue prior to 2016-17.

|

2016-17 |

2017-18 |

2018-19 |

||||||||||||||

|

First-tier Tribunal |

Upper Tribunal |

High Court |

Court of Appeal |

Supreme Court |

First-tier Tribunal |

Upper Tribunal |

High Court |

Court of Appeal |

Supreme Court |

First-tier Tribunal |

Upper Tribunal |

High Court |

Court of Appeal |

Supreme Court |

||

|

Total |

1130 |

78 |

15 |

28 |

4 |

1966 |

77 |

15 |

29 |

5 |

1642 |

59 |

8 |

31 |

5 |

|

|

Decision for HMRC |

867 |

62 |

10 |

19 |

2 |

1420 |

55 |

12 |

24 |

3 |

1029 |

42 |

7 |

20 |

4 |

|

|

Partial win |

79 |

3 |

1 |

3 |

0 |

104 |

2 |

2 |

2 |

1 |

204 |

4 |

0 |

3 |

1 |

|

|

Decision for customer |

184 |

13 |

4 |

6 |

2 |

442 |

20 |

1 |

3 |

1 |

409 |

13 |

1 |

8 |

0 |

|

|

HMRC Success rate |

84% |

83% |

73% |

79% |

50% |

78% |

74% |

93% |

90% |

80% |

75% |

78% |

88% |

74% |

100% |

|

|

2019-20 |

2020-21 |

|||||||||||||||

|

First-tier Tribunal |

Upper Tribunal |

High Court |

Court of Appeal |

Supreme Court |

First-tier Tribunal |

Upper Tribunal |

High Court |

Court of Appeal |

Supreme Court |

|||||||

|

Total |

1907 |

49 |

3 |

18 |

4 |

1052 |

53 |

3 |

17 |

5 |

||||||

|

Decision for HMRC |

1465 |

34 |

1 |

9 |

2 |

855 |

42 |

3 |

11 |

1 |

||||||

|

Partial win |

119 |

3 |

1 |

0 |

0 |

50 |

2 |

0 |

3 |

1 |

||||||

|

Decision for customer |

323 |

12 |

1 |

9 |

2 |

147 |

9 |

0 |

3 |

3 |

||||||

|

HMRC Success rate |

83% |

76% |

67% |

50% |

50% |

86% |

83% |

100% |

82% |

40% |

||||||

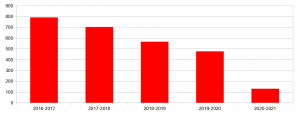

Criminal Investigations

In 2020-21 HMRC concluded 437 criminal investigations. This is compared with 864 in 2019-20, a 49% reduction, which HMRC states is due to Covid-19.

Between COP8, COP9, and criminal investigation, HMRC’s Fraud Investigations Service completed 1,217 investigations for tax fraud in 2020-21, down from 1,720 the previous year.

To put this into context, in the year before the pandemic, the Department for Work and Pensions (DWP) conducted 27 times more civil and criminal fraud investigations than HMRC in 2019-20.

HMRC have also provided us with data showing prosecutions for the ten years to 2019-20, showing a 91% average success rate in securing a conviction. While we do not know the full breakdown, it is clear that at least some o f these prosecutions are unrelated to tax fraud. Offences prosecuted include ones pertaining to the Immigration Act 1971 and the National Minimum Wage Act 1988.

|

FY |

Convictions |

Acquittals |

Prosecutions |

% Success |

|

2011-12 |

413 |

36 |

449 |

92% |

|

2012-13 |

540 |

36 |

576 |

94% |

|

2013-14 |

716 |

45 |

761 |

94% |

|

2014-15 |

642 |

67 |

709 |

91% |

|

2015-16 |

808 |

72 |

880 |

92% |

|

2016-17 |

807 |

79 |

886 |

91% |

|

2018-19 |

835 |

82 |

917 |

91% |

|

2019-20 |

648 |

101 |

749 |

87% |

|

2020-21 |

608 |

83 |

691 |

88% |

|

Total |

6017 |

601 |

6618 |

91% |

Convictions by year

Despite the reduction in convictions from 835 in 2018-19, to 648 in 2019-20, and 608 in 2020-21, the success rate has been trending downwards. The success rate peaked at 94% throughout 2012-13 and 2013-14, but now sits at 87% for 2019-20 and 88% for 2020-21.

Offences Charged And Reaching A First Hearing At Magistrates’ Courts

Figures obtained under FOI from the Crown Prosecution Service (CPS) demonstrate a clear decline in prosecutions for almost all forms of tax fraud. While the decline in 2020-21 is understandable given the pressures of the pandemic, that does little to explain the downward trend.

|

2016-2017 |

2017-2018 |

2018-2019 |

2019-2020 |

2020-2021 |

|

|

Common Law (Cheating the Public Revenue) |

144 |

113 |

127 |

79 |

19 |

|

Criminal Law Act 1977 { 1(1) } (Conspiracy to Cheat the Public Revenue) |

9 |

13 |

49 |

27 |

1 |

|

Taxes Management Act 1970 { 106A } |

173 |

127 |

62 |

69 |

21 |

|

Value Added Tax Act 1994 { 72(1) } |

228 |

184 |

161 |

129 |

48 |

|

Value Added Tax Act 1994 { 72(3)(a) } |

100 |

65 |

69 |

33 |

18 |

|

Value Added Tax Act 1994 { 72(3)(b) } |

17 |

1 |

0 |

1 |

0 |

|

Value Added Tax Act 1994 { 72(8) } |

1 |

3 |

2 |

1 |

0 |

|

Value Added Tax Act 1994 { 72(11) of and paragraph 4(2) of Schedule 11 } |

119 |

196 |

96 |

137 |

23 |

|

Total |

791 |

702 |

566 |

476 |

130 |

HMRC’s 2020-21 accounts state that due to Covid-19 there has been a significant reduction in the amount of criminal investigations closed. With fraud on the rise, HMRC requires more resources in order to deal with the significant increase in criminality.

Offences Charged And Reaching A First Hearing At Magistrates’ Courts

Positive Charging Decisions against the target of 100 prosecutions for serious and complex tax crime

In 2015, HMRC stated their aim to increase the number of prosecutions into serious and complex tax crime, focusing particularly on wealthy individuals and corporates. The stated aim was to increase prosecutions in this area to 100 by 2020-21.

|

2017-18 |

2018-19 |

2019-20 |

|

|

Positive Charging Decisions |

33 |

42 |

46 |

In February of 2020, HMRC told us that they were on track to meet the commitment by the end of 2019-20, however, the pandemic will have affected this work. HMRC used to publish this target in their annual report, however, it is missing from the 2020-21 edition. It is assessed as likely that HMRC will have missed the target this year.

S161 of Finance Act 2016, Tax Strategies and Sanctions for Persistently Uncooperative behaviour

In 2016, as part of the Government’s crackdown on tax dodging Parliament introduced ‘special measures’ for companies found to be persistently non-compliant. This was defined as persistently failing to disclose information requested by HMRC, or being a serial abuser of tax avoidance schemes.

When the government first consulted on introducing the measure in 2015 it pencilled in an additional £40m a year in tax being raised. By the 2016 budget, the government was expecting the measure, together with the requirement for large firms to publish their tax strategies, would bring in more than £500m a year.

In October 2019, TaxWatch revealed that zero companies had been put into special measures since the legislation was introduced.

On 31 August 2021, HMRC responded to a further FOI from TaxWatch, confirming that “To date HMRC has not issued any sanctions under s161 of Finance Act 2016 for persistently uncooperative behaviour”.

Covid-19

Department expects to recover 25% of the billions lost to fraud and error

As the pandemic spread, and with lockdowns presenting significant economic challenges to the UK, HMRC was tasked with delivering many of the government’s financial support schemes. These included furlough, the Self-Employment Income Support Scheme, and Eat Out to Help Out. Due to the speed in which these were rolled out, they were subject to widespread abuse, costing the UK government an estimated £5.8bn in fraudulent and erroneous claims.

Jim Harra, the head of HMRC, stated in an interview with the FT in November 2021 that the organisation will struggle to recover more than half of the losses to fraud and error to Coronavirus support schemes, and plans to recoup the money lost may not go beyond 2022-23.12

However, HMRC later published figures which showed that current estimates would see the department collecting no more than 25% of the amount lost to fraud and error.13

Taxpayer Protection Taskforce

In the March 2021 Budget Chancellor Rishi Sunak confirmed the creation of a £100m “Taxpayer Protection Taskforce”, to be staffed by 1,265 “HMRC operatives”, seeking to recoup money wrongly claimed from pandemic support schemes. With HMRC announcing on multiple occasions that it was not intending on hiring new staff to deal with fraud and error in Coronavirus support schemes,14 these 1,265 staff will have been moved from other departments. The first £100m is set to cover the 2021-22 financial year, with a further £55m announced at the Autumn 2021 Budget to cover 2022-23. At current we are unaware of any funding plans for the taskforce to cover April 2023 onwards.

By comparison, the DWP have been granted £613m to deal with Covid related fraud over three years.15

While it is important to have a dedicated body to deal with this large scale fraud and error arising out of Covid Schemes, HMRC has already acknowledged that it will have a detrimental impact on other areas of business, which are already overstretched and having to deal with vast changes following Brexit.16

Coronavirus Job Retention Scheme (CJRS)

With millions of people unable to work due to the pandemic, the UK government introduced the Coronavirus Job Retention Scheme (CJRS), which subsidised 80 per cent of people’s wages up to a maximum of £2,500 a month. Known as furlough, this scheme saved millions from unemployment.

HMRC estimate that around 8.7% of CJRS expenditure was claimed either fraudulently, or in error, equating to just under £5.3bn. Of this, it is thought that around £3.9bn is fraud.17 This is almost as much as HMRC estimates for ‘Hidden Economy’18 (£3bn) and ‘Avoidance’ (£1.5bn) combined.

Despite the scale of the issue, HMRC are sticking to their investigation policy of pursuing the vast majority of this fraud as a civil matter. Speaking to the BBC about furlough fraud, Janet Alexander, the head of the Taxpayer Protection Taskforce said:

“In the UK, we use civil powers to recover the monies, we don’t normally criminally prosecute – that is the way that we handle tax investigations in the UK. It doesn’t mean it’s not a fraud, it’s just not the way that we deal with it.”19

Despite HMRC receiving over 30,000 reports of potential furlough fraud by August 2021, only 20 of these investigations had led to criminal inquiries.20 These criminal prosecutions can and do lead to successful recovery of money – in October 2021 it was announced that HMRC had recovered £26.5m in furlough money that was claimed fraudulently from four non-existent businesses owned by one individual.21

Even pursuing this fraud and error as a civil matter, HMRC has a long way to go. It was revealed to a law firm via FOI that at the end of June 2021, HMRC had conducted 7,632 compliance interventions relating to fraud and error with CJRS22. These interventions are not necessarily leading to penalties. HMRC informed us on 13 August 2021 that “Since the start of the CJRS scheme, we have issued 50 penalties with a total value of £276,591.” While a step in the right direction, this is billions of pounds shy from the estimated total amount lost through error and fraud.

A further method for recovering incorrect payments is through companies voluntarily rectifying the matter. HMRC revealed to us that as of 18 February 2021, over 13,000 organisations had made over 15,000 repayments, at a total value of £446.5m. At the same time, 112,000 organisations had made over 145,000 “corrections”, for a total value of £262.2m.

Self-Employment Income Support Scheme (SEISS)

SEISS was established to support self-employed individuals and members of partnerships. While not subject to the same levels as furlough, HMRC estimate that around 2.5% of SEISS expenditure was claimed either fraudulently or in error, equating to around £493m.

By the end of June 2021, HMRC had conducted 6,351 compliance interventions into SEISS.23 No arrests have yet been made in relation to the SEISS scheme.

Eat Out To Help Out (EOHO)

In August 2020, the UK government ran the ‘Eat Out to Help Out’ scheme, which sought to attract customers back to restaurants by offering a 50 per cent discount per person per meal. The scheme cost around £840m. HMRC estimate that 8.5% of Eat Out to Help Out claims were fraudulent or in error, which equates to just over £71m. As the EOHO scheme was limited in that it only ran for a limited period in August 2020, estimates into abuse should be more accurate than those for CJRS or SEISS.

At the end of June 2021, HMRC had launched only 584 compliance interventions into EOHO.24 HMRC had previously announced in November 2020 that they were to contact around 4,000 hospitality businesses asking them to double check their Eat Out to Help Out claims. At 30 June 2021 there had been five arrests related to EOHO.

By comparison, earlier this year the Department for Work and Pensions (DWP) announced that they were to re-check a million Universal Credit cases for possible fraud as overpayments almost doubled during Covid to £8.4bn.

|

Total number of interventions and arrests as at 30 June 2021 |

||

|

Scheme |

Compliance Interventions |

Arrests |

|

CJRS |

7,632 |

5 |

|

SEISS |

6,351 |

0 |

|

EOHO |

584 |

5 |

Customer Service

Customer service is important for HMRC. If someone is trying to contact HMRC in order to pay their taxes, it is important that they are able to get through. Under-staffing and under-resourcing leads to taxpayers being unable to contact HMRC to pay their tax, or to correct any overpayments.

A lack of customer service can have the consequence of taxpayers questioning the effectiveness of the overall state of the tax system. This is particularly important for the self-employed who have to sort their own tax affairs.

Calls

The total amount of calls HMRC receives has decreased year on year since 2015. Though data is only available from 2018, while total call volumes are decreasing, the amount of people waiting longer than 10 minutes to speak to an adviser is increasing, doubling in the two years to 2020. That amount increases further, to 45%, in the 2020-21 year, though this can likely be accounted for due to the interruption of the pandemic.

|

Calls |

2011-12 |

2012-13 |

2013-14 |

2014-15 |

2015-16 |

2016-17 |

2017-18 |

2018-19 |

2019-20 |

2020-21 |

|

Call Volumes |

77,803,005 |

72,090,702 |

68,137,509 |

64,781,978 |

60,804,092 |

49,865,940 |

46,745,705 |

42,691,993 |

41,631,930 |

33,308,535 |

|

Average Speed of Answer |

04:38 |

04:00 |

04:24 |

09:45 |

11:54 |

03:54 |

04:28 |

05:14 |

06:39 |

12:04 |

|

% of call attempts handled by our Contact Centres |

74.3 |

75.1 |

78.8 |

71.9 |

71.6 |

91.7 |

87.1 |

84.1 |

79.4 |

73.6 |

|

% of customers waiting longer than 10 min to speak to an adviser |

– |

– |

– |

– |

– |

– |

14.6 |

19.7 |

29.9 |

44.7 |

Post

Moving to postal correspondence, the amount of post received by HMRC has steadily declined over the past eight years for which data are available. Despite this decline, there has been no major shift in the amount of mail that is cleared within 15 working days of receipt.

|

Post Volumes |

2011-12 |

2012-13 |

2013-14 |

2014-15 |

2015-16 |

2016-17 |

2017-18 |

2018-19 |

2019-20 |

2020-21 |

|

Post Volumes |

– |

– |

24,528,543 |

21,663,039 |

19,802,549 |

20,369,531 |

18,180,451 |

19,029,213 |

17,293,593 |

15,693,910 |

|

% of post received by HMRC that has been cleared within 15 working days of receipt |

66.0 |

85.0 |

83.0 |

70.0 |

52.2 |

81.0 |

80.7 |

76.6 |

70.3 |

64.4 |

|

% of post received by HMRC that has been cleared within 40 working days of receipt |

– |

– |

– |

– |

87.0 |

96.3 |

97.1 |

96.4 |

88.0 |

85.3 |

Complaints

HMRC operates a formal two-tier complaints process. Tier 1 is HMRC’s first attempt to resolve a complaint. If a person is not satisfied with the response at Tier 1, they can ask for the complaint to be looked at again and this becomes a Tier 2 complaint.

No obvious trend emerges in the past decade of complaints, other than that the number of Tier 2 complaints has declined from a high in 2012-13. However, it should be noted that the amount of complaints upheld are relatively high, with 43% of tier one complaints being either partially or fully upheld.

|

Complaints |

2011-12 |

2012-13 |

2013-14 |

2014-15 |

2015-16 |

2016-17 |

2017-18 |

2018-19 |

2019-20 |

2020-21 |

|

Tier 1 number of complaints received |

74,831 |

67,956 |

64,729 |

74,427 |

80,391 |

77,279 |

77,410 |

71,638 |

65,625 |

78,542 |

|

Tier 1 % fully upheld |

31.0 |

25.0 |

32.0 |

31.0 |

34.0 |

33.0 |

39.0 |

36.0 |

35.5 |

28.9 |

|

Tier 1 % partially upheld |

14.0 |

12.0 |

13.0 |

15.0 |

17.0 |

16.0 |

14.0 |

16.0 |

16.9 |

14.5 |

|

Tier 2 number of complaints received |

8,754 |

11,751 |

6,895 |

7,513 |

6,186 |

5,339 |

5,006 |

5,209 |

4,431 |

5,802 |

|

Tier 2 % fully upheld |

19.0 |

21.0 |

57.0 |

33.0 |

26.0 |

19.0 |

19.0 |

19.0 |

22.4 |

13.4 |

|

Tier 2 % partially upheld |

15.0 |

12.0 |

11.0 |

17.0 |

23.0 |

25.0 |

22.0 |

22.0 |

26.4 |

16.0 |